Altria Q1 2024 results - implications for BAT / PM / IMB

Altria Q1 2024 results - implications for BAT / PM / IMB

MO 0.00%↑ BTI 0.00%↑ PM 0.00%↑ $IMBBY

I don’t own any shares in Altria but I still monitor its quarterly performance from time to time to benchmark against my other investments such as BAT, PM, IMB. Altria recently announced its Q1 2024 results and an article on Tobacco Insider well summarised the key takeaways. I suggest you taking a look at the Tobacco Insider article first as it contains details that serve as backdrop of what I am going to write. Then I would like to switch the gear to analyse the result from its competitors’ perspective and try to triangulate the operating data. Here we go.

BAT - cigarette segment in the U.S.

Similar to Altria, BAT’s cigarette segment is also over-indexed to the premium segment, hence negatively impacted by macroeconomic pressure and downtrading trend in the U.S. What differentiates Altria from BAT is that Altria has a price laddering structure through Marlboro Black which is cheaper version of Marlboro that allows consumers to stay within the Marlboro family during economic recession. BAT didn’t have a sister brand for its premium Newport brand and instead decided to launch Lucky Strike in 1H 2022, a discount brand in the U.S. to counter the downtrading trend. However the downside of the strategy is that once consumer downtrades to another brand, it may not be straight forward for them to return to Newport when economy recovers. It is neither straight forward for a Newport customer to switch to Lucky Strike during economic downturn, as they have many other deep discount brands to choose from, such as Liggett Select, Pyramid, Eagle 20's, Eve, Montego, and Grandprix marketed by Vector Group. Hence in 2023, BAT tried to follow suit and activated commercial plan for “soft pack” version of Newport which is cheaper than the normal Newport product to mitigate the downtrading impact. While BAT demonstrated some success in its Newport soft pack and Lucky Strike, all in all, it looks like Altria still outperforms BAT in the smokable segment in terms of value share as Nielsen IQ data suggests.

Looking at Altria’s Q1 numbers, it seems Marlboro is gaining share in the premium segment, likely at the expense of shares ceded by Newport. However, one quarter’s number may not mean a lot as it could be affected by shipment and inventory level at retail channel. Altria’s share of wholesale inventory increased from 30.9% at the end of Q1 2023 to 35.6% at the end of Q1 2024, probably contributing to +0.7pp yoy increase in Marlboro share of the premium segment to certain extent. As Marlboro raised its retail price twice thus far year to date, which increased the price gap against other brands and even Newport, investors may doubt whether it can continue to hold its market share in the premium segment. A wild card here is Altria’s robust revenue growth management (RGM) infrastructure, which allows it to implement various levels of pricing even within the same city, so the price of Marlboro purchased in one store would be different from another store located elsewhere, taking into account different levels of price elasticity among different consumers.

BAT - ecig segment

Altria’s Njoy brand has aggressively expanded distribution network, resulting in +1.1pp share gain from Sep 2023 to Mar 2024. There’s not much evidence suggesting repeated purchase may sustain the growth momentum. Using PMI CEO’s language, Njoy is still playing a game of “being big”. Will need to monitor the next few quarters numbers to see how it goes. Thus far, Njoy has not posed a threat to Vuse’s market leadership in the pod-based vaping segment.

Still, the biggest issue facing BAT’s Vuse is the proliferation of illicit disposable vapes, which shall continue to haunt the pod-based vaping market. Altria doesn’t assume any improvement in such aspect when assessing the full year guidance amid inadequate enforcement actions taken by the FDA. It has advised FDA specific steps to address the illicit market and collaborated with various state legislatures to enact “PMTA Registry Bill”. A signpost would be the marketplace dynamics in Lousiana, which is one of the first states passing such bill. Will need more time to monitor the outcome when such bill becomes effective in other states later this year.

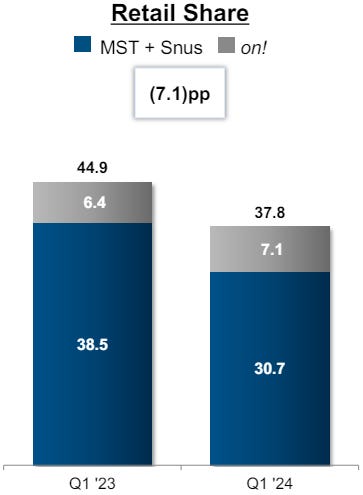

PM - oral tobacco segment

Altria’s retail share in the oral tobacco segment declined by 7.1pp yoy, as growth in on! was more than offset by decline in moist snuff + snus segment. Even within the modern oral segment, on!’s market share also shrinks as the category growth is led by ~80% growth of ZYN yoy, whilst on! only grew by 32%. Zyn is the undisputed leader in the modern oral segment and PM may soon overtake Altria’s leadership in the oral tobacco segment (modern oral + snus + moist snuff). The only concern here is the explosive growth may draw negative publicity and be politicised, resulting in litigation or stricter regulation. If it happens, Zyn could share the faith of Icarus, who perished by flying too near the Sun with waxen wings.

IMB - cigarette segment

While IMB is gaining market share in the U.S. due to its presence in the branded discount segment amid downtrading trend, some investors may doubt how sustainable it can be. If we breakdown the discount segment by branded discount and deep discount, actually downtrading trend mainly benefits the deep discount segment. Downtrading has accelerated since Q3 2023, evidenced by 0.4pp share gain of deep discount segment per quarter sequentially since then.

In the recent pre-close trading update, IMB claimed it was on track to meet half-year and full-year guidance. According to the latest Nielsen data, IMB is still gaining volume and value share in the U.S. cigarette segment, despite the branded discount segment as a whole doesn’t gain share. I believe it is mainly because IMB’s big tobacco peers are focused on defending market share in the premium segment. In fact, Altria’s shipment volume in the discount segment decreased by 30% yoy in Q1 2024. BAT’s Pall Mall brand, also positioned as a branded discount product, saw its volume declining by ~25% yoy according to the latest Nielsen data. Hence IMB’s success in the U.S. cigarette market is not solely attributable to the downtrading trend, but rather it has executed the right strategy as a challenger.

Conclusion

Despite headwind from illicit market and macroeconomy (rising credit card deliquency rate, stagflation etc.), U.S. is still the most profitable nicotine market outside of China. It is interesting to see how the key players play their hands to make as much profit as possible. PM stands out as the key beneficiary of the prevailing market trends as it doesn’t have the burden of a cigarette business in the U.S.

But as always, a good company doesn’t neccessarily mean a good investment. To be fair, Altria, BAT and IMB are not fooling around and acting recklessly. One has to look at the relative valuation and compare it to operating metrics to ascertain how much growth and risk are priced in. It is not that easy to find mispricing opportunity in the tobacco sector.

> Hence IMB’s success in the U.S. cigarette market is not solely attributable to the downtrading trend, but rather it has executed the right strategy as a challenger.

Stefan Bomhard has repeatedly said Imperial needed a “challenger” mindset in order to compete with its larger rivals.

IMB > BAT > PM > MO