BAT - ITC stake disposal thoughts

BAT recently disposed of a 2.5% stake in ITC Limited to realise GBP1.05bn proceeds, of which GBP200m will be deployed for share buyback in FY25, bringing the total to GBP1.1bn for the year. I would like to share with you my thoughts about this transaction. Before I provide any comment, let’s take a look at how this transaction started and what happened in 2022-2023.

Key events in 2022-2023

There are three factors contributing to the recent sell-down, as well as the GBP1.57 billion disposal in March 2024.

Surge of ITC Limited stock price since 2022, driven by robust volume and pricing growth of cigarettes in India, where ITC holds close to 80% market share in the legal cigarette market in India. This is driven by the post-COVID economic recovery in India, a modest excise tax environment, and enhanced enforcement against illicit cigarettes, which enables the legal cigarette industry to partially claw back volumes from illicit trade. To give you an idea of how dire the situation was before 2022, let’s take a look at ITC’s disclosure in its FY22 annual report.

While India is the world’s second largest consumer of tobacco, legal cigarettes constitute only 8% of overall tobacco consumption in India, as against a global average of 90%. It is pertinent to note that India accounts for less than 2% of global cigarette consumption despite comprising 18% of the world’s population, making India’s per capita cigarette consumption amongst the lowest in the world.

Over the years, discriminatory and punitive taxation on cigarettes has led to progressive migration from consumption of duty-paid cigarettes to other lightly taxed/tax-evaded forms of tobacco products, comprising illicit cigarettes and bidi, chewing tobacco, gutkha, zarda, snuff, etc.

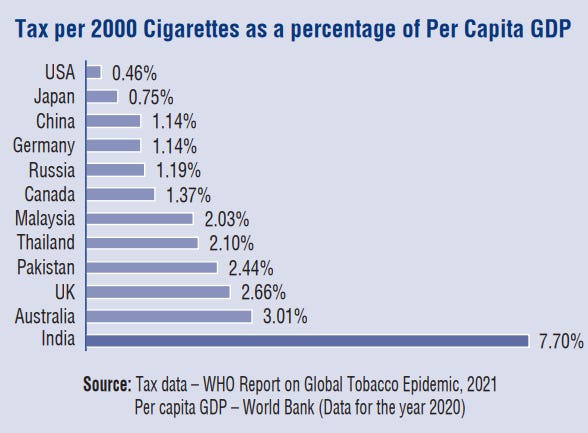

Taxes on cigarettes are one of the highest in India as depicted in the chart.

Taxes on cigarettes in India are multiple times higher than in developed countries viz. 17x of USA, 10x of Japan, 7x of Germany and so on. Further, the same is also substantially higher than that in neighbouring countries. It is pertinent to note that India’s per capita cigarette consumption is amongst the lowest in the world and is significantly lower compared to that of China, Japan, USA, UK and even neighbouring countries such as Bangladesh and Pakistan.

During the period 2012-13 to 2016-17, excise duty on cigarettes increased sharply at a CAGR of 15.7%; however, tax revenue from cigarettes grew by a mere 4.7% CAGR during the same period. In 2017-18, the legal cigarette industry was further impacted by a sharp rise of 20% in tax incidence as a result of increase in excise duty and transition to the GST regime.

Thereafter, relative stability in taxation until January 2020 helped the legal industry partially claw back volumes lost to the illicit trade in earlier years; consequently, revenue collections witnessed a marked buoyancy growing by 10.2% during this period.

In 2022, there were four notable events, somehow forming a perfect storm, putting BAT’s net-debt-to-EBITDA ratio and worsening credit metrics in the spotlight.

BAT started a GBP2bn share buyback program, which was announced in Dec 2021.

Russia’s military incursion into Ukraine in Feb 2022, forcing BAT to retreat from Russia and Belarus markets, forgoing 3.1% of its revenue and 2.4% of its EBIT.

The interest rate hike cycle initiated by the U.S. Fed began, resulting in increased interest expenses for BAT upon refinancing its debt.

Major credit agencies have placed BAT on a negative watchlist due to the events mentioned above, putting it at risk of a credit rating downgrade unless there is an acceleration of deleveraging.

The BAT share price tanked in 2023, falling below the COVID-19 level, driven by disappointing U.S. performance. This was mainly due to the proliferation of illicit disposable vapes and ZYN’s explosive growth, which accelerated cross-category movement, resulting in a double-digit volume decline of cigarettes, deceleration of VUSE growth, and VELO losing competitiveness. Also considering the threat of a menthol ban in the U.S., BAT decided to recognise a £27.6 billion non-cash impairment charge mainly relating to its U.S. business. In stark contrast, the ITC share price went in the opposite direction and almost tripled the multi-year low recorded during COVID. To put it in perspective, BAT’s 29% stake in ITC was worth GBP16bn in Dec 2023, accounting for 30% of BAT’s market cap but ~7% of BAT’s adjusted net profit (excluding goodwill impairment and intangible asset amortisation of BAT’s U.S. brands).

If BAT decided to sell its entire stake in ITC and deploy the proceeds for share repurchase, it could reduce its share count by 30% (based on the Dec 2023 share price of BAT) and net profit by ~7%, thereby increasing earnings per share by 39% and reducing dividend payout ratio from ~65% to ~47%, resulting in ex-dividend free cashflow of GBP4bn available for deleveraging and share buyback. As you can imagine, the rising share price of ITC made BAT shareholders and analysts quite uneasy. Thus, BAT was under immense pressure to unlock value from its ITC stake.

Below is extracted from BAT’s 2023 First Half Pre-Close Conference Call. Nik Oliver, the UBS analyst, asked a billion-dollar question, “The sell-down of ITC stake - if not now, when?” (note: he didn’t use such language, but I try to translate his British English to simplified English that everyone can relate to) As expected, BAT CEO Tadeu Marroco answered with some reservations in a rather British manner.

Nik Oliver, UBS

……And then the second one is just regarding the investment in ITC. You know that has been asked quite a lot by investors recently given the relative valuations, but just any comments on how you think about that investment and whether there is any scope to increase value from that investment over time? Thank you.

Tadeu Marroco, Chief Executive

……And your other question on the ITC. Look our stake in ITC is regularly assessed by the Board. But there is one point that we have to take into consideration. There are significant regulatory and bureaucratic hurdles to overcome. For example, we have a foreign direct investment ban in tobacco in terms of regulation, RBI processes, if you were to monetise some of our shareholding in ITC it is not that straightforward as you could imagine. That is the first point.

The second is that for sure we consider the investment in ITC at this stage more than a financial investment. We consider it a strategic one. And why do we do that? Well first of all because of the size of the Indian market, the largest population in the world today. And more importantly the established oral markets that we have in India. Volume wise, if you consider all the volume of the oral consumption in India it is higher than the consumption of oral elsewhere in the world. Just to give you an idea.

So, we believe that we might have significant opportunities in terms of New Categories, mainly in the oral space, in India over time.

So, for sure ITC is also doing extremely well, it is a very valuable asset. We have been – you know very pleased with the performance in terms of dividends, in terms of the share price. And there is a still a long gap in terms of valuation of ITC compared with other FMCGs in that market, which means that there is a lot of potential for growth in the future.

So, I just want to make all these points clear for everyone on the call as well regarding ITC.

Key events in 2024-2025

BAT’s decision to sell GBP1.57bn worth of ITC stake in Mar 2024 may be driven by the above backdrop. However, I wasn’t sure whether it was committed to selling more, as it retained slightly more than 25% stake in ITC Limited after the disposal, a minimum threshold required for keeping its veto rights. As mentioned by Tadeu Marroco during the 2023 preliminary results conference call, BAT sought to maintain its level of influence in the ITC, which was transforming in response to local legislation. Hence, BAT considered the veto rights to be essential for the time being.

The recent GBP1.05bn sell-down may look like a smaller amount, but it was more significant from a strategic point of view, as BAT finally gave up the veto rights in ITC after its shareholding dropped below the 25% minimum threshold. It implies that further sell-down is possible, and ITC may be treated as a financial investment rather than a strategic investment over time (maybe not immediately).

In hindsight, the Canadian tobacco litigation may have been a catalyst. Following the imminent USD3.5bn upfront payment to settle Canada’s legal claim and ongoing annual payments (based on 85% of net income after taxes, excluding that generated by alternative nicotine products), BAT’s net debt to EBITDA will be increased by 0.3-0.4x. Against this backdrop, BAT still commits to be back within its target leverage range of 2-2.5x net debt to ETBIDA post court approval and implementation of the proposed plans by the end of 2026. Without the recent ITC stake disposal, it is still achievable but BAT will have little margin of error, i.e. it must return to its medium-term algorithm of 3-5% revenue and 4-6% adjusted profit from operations growth on a constant currency basis by 2026. With the recent ITC stake disposal, BAT’s net debt would be reduced by GBP850m, or 0.07x EBITDA, creating breathing room in its deleveraging journey.

Conclusion

More importantly, once the target leverage range is reached, further disposal of the ITC stake can be fully deployed for share buyback instead of deleveraging. The remaining ITC stake is worth ~GBP10bn based on the current share price. If fully deployed for share buyback, it would reduce BAT’s share count by ~14% and net profit by ~5%, hence EPS accretion of ~10-11% on a pro forma basis. It will reduce the dividend payout ratio from ~68% to ~61%, creating more flexibility for a combination of dividend growth (BAT may still commit to a 65% dividend payout ratio over the long term), share buybacks (perhaps an evergreen buyback of GBP1.5-2bn per annum?), and deleveraging (if BAT wants to get to the lower end of its target leverage range and obtain a single-A credit rating). It could slow down BAT’s organic growth (as measured by adjusted profit from operation) though, due to ITC’s faster growth than the rest of BAT, which is not that bad if it leads to a lower P/E ratio of BAT (if P/E ratio is positively correlated to profit growth) allowing more shares to be repurchased given the same amount allocated for share buyback, hence EPS growth and total shareholder return % (dividend yield + EPS growth, assuming constant P/E multiple) may not be meaningfully affected.

While a full disposal is unlikely to occur, the narrative that ITC becomes a financial investment rather than a strategic investment may imply that BAT can be valued on a sum-of-the-parts basis, thereby separating the valuation of ITC from other segments. Why does it matter? The majority of Wall Street analysts currently value BAT based on a P/E multiple assigned to the group's earnings or an EV/EBITDA multiple assigned to the group's adjusted EBITDA, minus net debt and minority interest. Let’s use P/E multiple as an example, BAT is currently trading at 9.45x 2025e P/E (using Vuma consensus estimate of GBP352.2 pence adjusted EPS, excluding Canada and assuming constant currency). ITC’s FY26e (fiscal year ending March) net profit is GBP1.9bn based on the consensus estimate, i.e. contribution to BAT earnings is roughly 22.9% x GBP1.9bn = GBP435mn. Applying 9.45x P/E to GBP435mn = GBP4.1bn, which is the implicit valuation of ITC reflected in the current valuation of BAT. This compares to GBP10.4bn value of BAT’s remaining stake in ITC, representing a GBP6.3bn gap between the two numbers. In anticipation of further sell-down of ITC and when it gets materialised over time, the GBP6.3bn gap could be gradually closed, representing 8.6% of BAT’s latest market cap.

However, I wouldn’t be presumptuous to conclude that BAT shall be worth 8.6% more than its current market cap based on the above calculation, as I have little faith in the capital allocation effectiveness of most public companies. To be conservative, I think the best-case scenario is that BAT continues to sell down its ITC stake gradually over time to support a more meaningful buyback program, while maintaining a significant minority stake in ITC to capture future growth opportunities in oral nicotine products in India, if and when the regulatory environment in India allows. The base-case scenario? As usual, BAT may only sell down ITC whenever it needs to offset deterioration in credit metrics and “smooth out” its P&L and balance sheet due to scheduled events (e.g. Canada tobacco litigation) or unexpected headwinds (e.g. Russia-Ukraine war, menthol ban, proliferation of illicit disposable vapes).

I consider the potential 10-11% EPS accretion or 8.6% share price appreciation as adding to the margin of safety, rather than treating these as immediately realisable upside potential. By the way, does this dynamic sound familiar to you? Suppose Altria didn’t lose billions of dollars from its failed JUUL and NJOY investment (the JUUL failure also created a tax shield arising from the partial release of a valuation allowance on JUUL-related losses). Would it still sell down its minority stake in ABI? If IMB didn’t experience market share loss for years and failed badly in its NGP investments, would it still sell its premium cigar business? (By the way, IMB may have sold its premium cigar business at a dirt-cheap price if you notice the pricing of premium cigar brands like Cohiba more than double or triple shortly after the transaction, while maintaining an incredibly strong demand. But this is a long story that I won’t elaborate further in this article.) This is also true for many other large-cap companies.

I hope you enjoy reading this article. BAT will publish its 2025 First Half Pre-Close Trading Update on Tuesday 3 June 2025 at 7.00am BST and will be followed by a short conference call and Q&A session hosted by Tadeu Marroco, Chief Executive, Soraya Benchikh, Chief Financial Officer, and Victoria Buxton, Group Head of Investor Relations at 8.30 am BST. Following that, I will publish an article to share my thoughts. To give you a hint of what I am going to write in the next article, it has something to do with the numbers highlighted in the table below, extracted from BAT’s FY21 annual report.

Thank you for the good article, Anthony. Has BAT mentioned how much tax they will pay on the capital gain? Claude and ChatGPT both come up with an estimate in the 10-15% range but there are many considerations.