Diageo's Turnaround: A Problem Well-Defined is a Problem Half-Solved

In an age where artificial intelligence can generate solutions at unprecedented speed, the most valuable human skill is no longer just problem-solving; it is problem definition. The quality of any answer, whether from a machine or a management team, depends entirely on the quality of the prompt. This is why the shift underway at Diageo is so compelling. After years of chasing complex and sometimes conflicting goals, the leadership team is finally defining the right problems with surgical precision, and that clarity is the most promising signal for a potential turnaround.

In my March article, “Diageo - a value stock or value trap?”, I laid out the case for why a titan of the spirits industry was trading at a deep discount. The diagnosis pointed to a handful of critical issues: alarmingly low free cash flow (FCF) conversion, a bloated capital expenditure program, soaring working capital tied up in maturing inventory, and a management incentive structure that seemed to reward growth at any cost.

The FY2025 preliminary results, while not stellar, were accompanied by a level of candour that suggests the diagnosis has been accepted. The new leadership is not just treating symptoms; they are addressing the root cause. This has given me the conviction to increase my position, fully aware that while the problems are now defined, solving them is far from guaranteed.

FY2025 Results: Treading Water, But Not Sinking

On the surface, Diageo reported a lacklustre FY2025 results (though less than feared). Reported net sales were flat at $20.2 billion, and reported operating profit plunged due to significant impairment and restructuring costs. Organic net sales grew by 1.7%, driven by a balanced 0.9% volume growth and a 0.8% positive price/mix.

Key financial highlights include:

Adjusted EPS: 164.2 cents, an 8.6% decline but slightly ahead of consensus.

Free Cash Flow: Increased to $2.7 billion, a positive sign supported by better working capital management.

Leverage: Net debt to EBITDA reached 3.4x, up from 3.0x the previous year but in line with guidance.

FY2026 Outlook: Diageo expects organic sales growth similar to FY25, but with organic operating profit growth accelerating to a mid-single-digit rate, and a robust FCF target of around $3 billion.

The market is right to be cautious. At ~15x P/E multiple, the current valuation demands a clear path to growth acceleration. A solid dividend alone won't deliver the total shareholder return investors expect. If EPS growth stalls, the valuation multiple could contract further, offsetting the 4% dividend yield to result in a negative return easily. The critical question, therefore, is how Diageo plans to reignite its growth engine.

The Nik Jhangiani Effect: A Culture of Candor and Accountability

The most profound change at Diageo isn't in the numbers yet; it's in the culture. For years, the company appeared to be managed by a set of rigid KPIs, with a particular “obsession” as Jhangiani himself calls it. For example, gross margin percentage. This fixation led to perverse outcomes, where profitable, volume-driving opportunities were ignored if they threatened to dilute the overall margin percentage. It is an example of letting metrics dictate strategy, rather than the other way around.

Jhangiani’s public statements have been resetting expectations and signalling a new era of commercial pragmatism. Consider this anecdote he shared about a discussion with the President of the North America division, which speaks volumes about the cultural shift he is driving:

"Laura came in and we were talking about RTDs and an opportunity to unlock growth in North America... And she started out with a question... she said so what gross profit margin do we want to achieve? And I said it's not about what gross profit margin we want to achieve, what's the accretive gross margin dollar pool that we can actually bring in that we are not playing in today and then the gross margin percentage is going to be the outcome of it.”

This is not just a semantic difference; it's a fundamental rewiring of the company's operational DNA. He was even more direct when linking this flawed thinking to the company's incentive structure, a core issue I highlighted in my previous article:

"I'm a firm believer around if you have the right metrics and you are measuring those, to deliver those, you need to incentivise them as well... I think the challenge has really been, it's potentially driven some wrong behaviours or some wrong choices in terms of where we want to play or not play because of margin percentage..."

This is the kind of bold, transparent leadership that was needed. It signals that the board has empowered him to make uncomfortable but necessary changes, starting with how management is compensated and held accountable.

A Complex Portfolio in a Shifting World

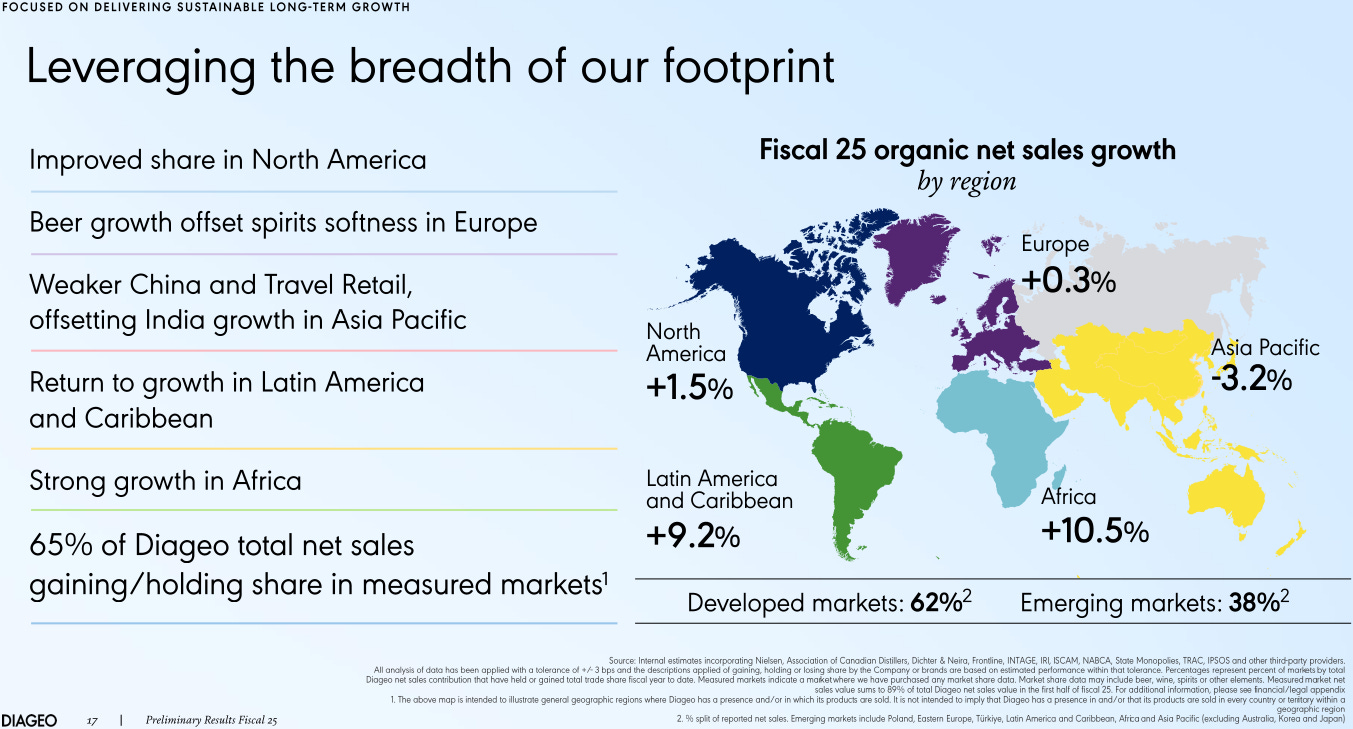

This new focus is critical because Diageo is navigating a complex and divergent global market. The latest results paint this picture clearly. The business derives 62% of its revenue from developed markets and 38% from emerging markets, a geographic diversification that is both a strength and a challenge. Performance was resilient in Africa and Latin America, but sluggish in the core markets of North America and Europe, and outright poor in Asia Pacific.

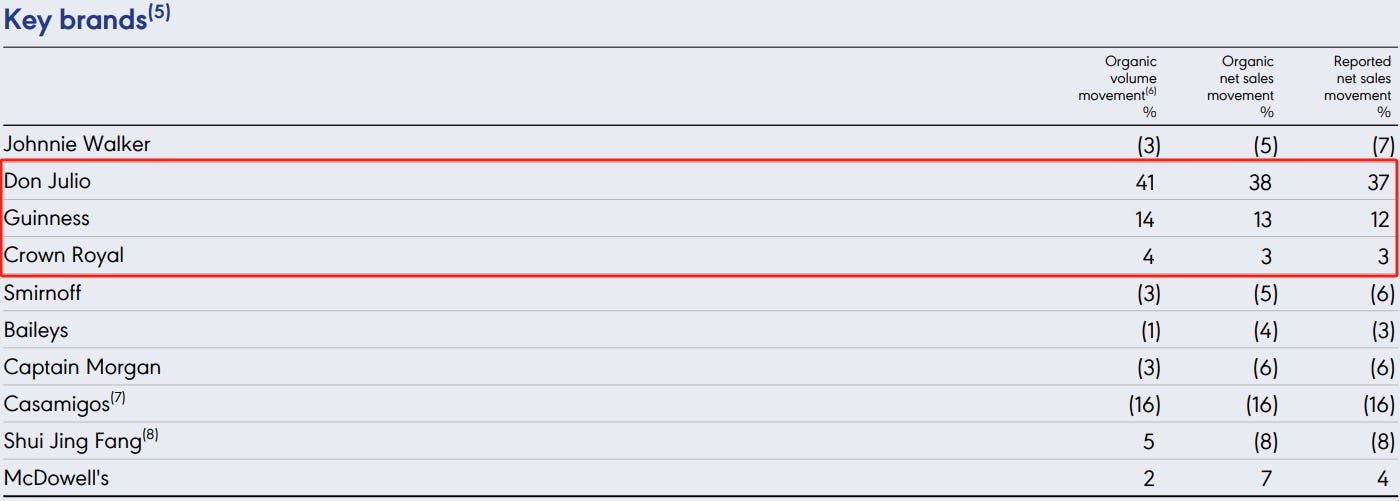

On the brand level, a few stars are carrying the weight. Guinness, Don Julio, and Crown Royal are driving growth, while many other brands in the portfolio are struggling against tough market conditions. This diversification across geographies and categories, each with its distinct landscape, makes predicting near-term momentum a fool's errand, even for management. The explosive, almost cultural-phenomenon growth of Guinness in recent years, for instance, owes as much to an organic and unpredictable shift in consumer tastes as it does to any specific management initiative.

While we cannot rely on luck, we can rely on sound capital allocation. The most reliable long-term strategy in such a complex environment is to focus investment on the largest and most profitable pools while driving for capital efficiency. This is precisely the shift in thinking that management is now championing.

Tackling the Financial Drags with Precision

With this new mindset, Diageo is now surgically addressing the financial issues that have weighed on its performance and valuation.

1. Taming the Capex Beast:

Diageo's capital expenditure reached an unsustainable 7.7% of net sales in FY25. This is nearly double the historical norm of ~4% seen before 2022, a period of aggressive expansion that was poorly timed with the subsequent market slowdown. The inflexion point is finally here. Management has explicitly guided for CapEx to fall over the next three years toward a mid-single-digit percentage of net sales. FY26 capex is guided to be $1.2-1.3 billion, down from $1.5 billion in FY25. This reduction alone is expected to drive a $200-300 million increase in FCF in FY26, providing a powerful and highly visible boost to cash generation.

2. Unlocking Cash from Maturing Stock:

Investment in maturing stock has been a massive FCF headwind. The cash flow statement reveals a $368 million cash outflow for maturing inventories in FY25. While this was down from the even larger $577 million in FY24 and $693 million in FY23, it represents a significant drain on capital. As these investments normalise and the aged liquid is eventually bottled and sold from FY27 onwards, this FCF headwind will transform into a multi-year earnings tailwind.

3. A Smarter, More Efficient Growth Engine:

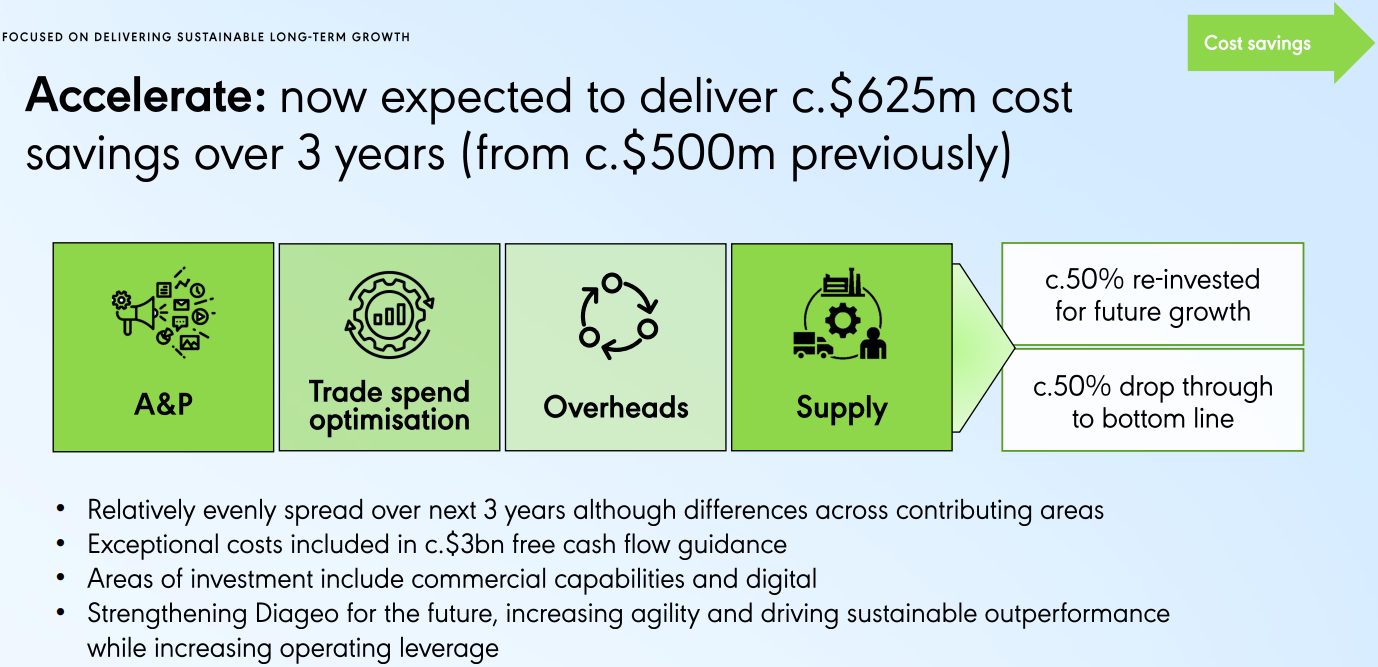

The “Accelerate” cost-cutting program has been upsized from $500 million to $625 million annually, with half flowing to the bottom line. Critically, this is not a blunt cost-cutting exercise. A key focus is making A&P spending more efficient. By leveraging AI and data analytics, Diageo reduced non-working media development costs from 21% of A&P in FY24 to 14% in FY25, with a clear goal of reaching ~10%. This is about reinvesting smarter, not just spending less.

The Path Forward: A Strategy of Balanced Growth

The singular focus on premiumization is evolving into a more pragmatic, balanced portfolio strategy designed to capture growth where it exists.

The clearest example is Guinness. The brand is on fire globally, but growth has been capped by supply. The new brewery being built in Kildare, Ireland, is a game-changer, set to increase total Guinness production capacity by 30% when it comes online in the second half of 2026. This will not only satisfy pent-up demand in core markets like the UK, Ireland, and the US but also fuel the international expansion of both classic Guinness and Guinness 0.0.

This balanced approach extends to tequila, where the company is moving beyond its ultra-premium focus to compete in broader, high-volume segments, and to RTDs, where innovation is meeting consumer demand for variety in flavour, ABV, and calories.

Conclusion: A Calculated Bet with Acknowledged Risks

After the results, Diageo's shares trade at a P/E multiple of approximately 15x, based on the announced adjusted EPS of 164.2 pence and the recent share price. This mid-teens multiple feels fair, pricing in both the challenges and the potential for recovery. It is a world away from the high-single-digit multiples of tobacco stocks we saw in recent years, but Diageo no longer carries the premium of a flawless growth compounder.

This is why I see the risk-reward as balanced. My decision to buy more shares is a calculated bet on the success of this turnaround, but I am not blind to the execution risks.

Can they execute a “balanced” strategy without diluting the premium brand equity they have spent decades building? Venturing into lower-margin, higher-volume categories is fraught with peril if not handled carefully.

Will the A&P efficiency drive be truly “smarter”, or will it devolve into simple cost-cutting that starves brands of the investment needed to maintain their cultural relevance?

External headwinds remain. A deteriorating economic environment could accelerate consumer downtrading beyond what even a more balanced portfolio can capture, even if Diageo fully absorbs the U.S. tariff on imports without passing it through to customers.

U.S. market share recovery, after a strong first half, is overshadowed by a sequential decline in the second half of FY25. While Don Julio, Guinness and Crown Royal continue to drive growth, there is more work to do with other brands.

Diageo is not an easy investment today. The path to restoring its status as a top-quartile TSR company will be challenging. However, for the first time in years, the leadership team has correctly identified the problems and is implementing a credible, financially disciplined plan to solve them. The inflexion point on capital allocation is here, and the culture is changing for the better. The ship is turning, and I am willing to bet it is turning in the right direction.

Great post. Thanks for sharing

Great post , thanks