Evolution AB: When a Growth Darling Becomes a Compounding Machine

For years, Evolution AB has been the undisputed king of the iGaming world and a darling of growth investors. As the pioneer and dominant force in the high-margin Live Casino segment, its ascent was nothing short of breathtaking. However, the narrative has shifted. A confluence of regulatory headwinds, slowing growth, and disappointing acquisitions has seen its valuation compress to historical lows, leaving many to wonder if the golden era is over.

While the market mourns the loss of a hyper-growth story, it may be overlooking the birth of something else: a resilient, cash-gushing compounding machine. This article will break down Evolution's formidable business model, address the "wall of worry" currently facing the company, and present a contrarian view: that at today's valuation, Evolution offers a compelling total shareholder return story that growth-focused investors are missing.

1. The House Always Wins: Evolution’s Business Model

The global iGaming market is a vast and growing space, projected to expand at a double-digit CAGR. Within this ecosystem, Evolution operates on a B2B2C model. It does not deal with end-players directly; instead, it provides fully integrated Live Casino solutions to online gaming operators (its customers), including Bet365, FanDuel, DraftKings, Entain etc.

The model is simple and powerful: Evolution builds and operates state-of-the-art studios, hires and trains professional game presenters, and streams high-quality, interactive casino games—from Blackjack and Roulette to its famous entertainment-centric game shows like Crazy Time—24/7. In return, it typically takes a ~10% revenue share from the gross gaming revenue generated by its customers.

The value proposition is clear: For casino operators, Evolution offers a capital-light, turnkey solution to provide their players with the most engaging and trusted Live Casino experience, a critical tool for user acquisition and retention.

2. A Formidable Moat in a Competitive Arena

Evolution's primary competitors are giants like Playtech and Pragmatic Play. However, Evolution has built a formidable moat that differentiates it significantly:

Unmatched Scale and Quality: With over 20 studios globally and thousands of game tables, the scale of its operation is unrivalled. This allows for immense game variety and linguistic localization, catering to a global player base. The production quality, from the studio design to the professionalism of the dealers, sets the industry standard.

Innovation in Game Shows: Evolution revolutionized the space by creating a new category of "game shows" that blend traditional casino mechanics with interactive entertainment. These games, which are difficult to replicate, act as powerful player acquisition funnels.

Technological Reliability: Providing a seamless, low-latency stream to millions of concurrent users is a significant technical challenge. Evolution's years of operational excellence have built a reputation for stability and trust that is paramount for its B2B customers.

3. A Look Under the Hood: Financial Performance

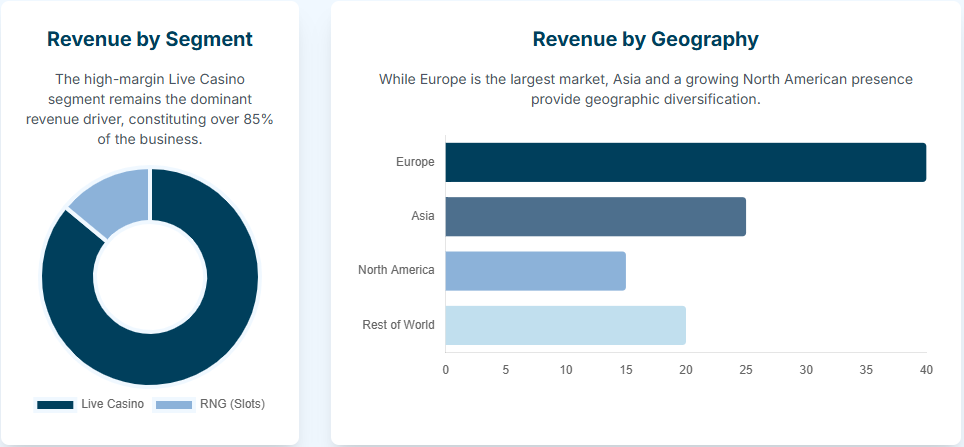

As of its latest reporting, Evolution’s revenue is dominated by the high-margin Live Casino segment, which constitutes over 85% of the business. The remainder comes from its RNG (Random Number Generator) or "slots" business, primarily built through acquisitions.

Geographically, Europe remains its largest market, but significant revenue is generated from Asia and a growing contribution from North America.

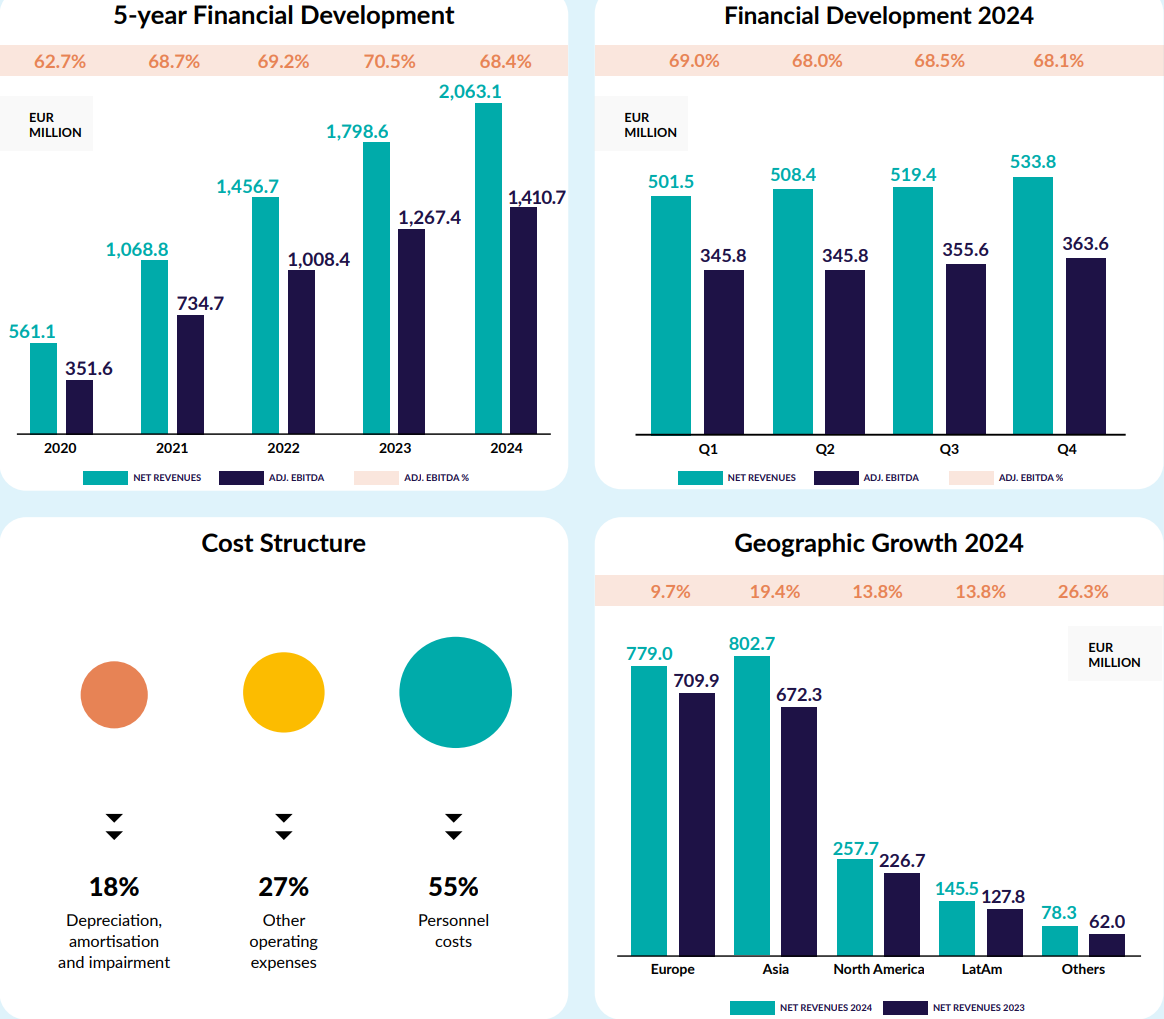

EBITDA Margin & Key Drivers: Evolution's profitability is exceptional, with historical EBITDA margins approaching 70%. This is driven by a powerful business architecture:

Geographic Arbitrage: It generates revenue from players in high-income countries (Europe, North America) while basing its labour-intensive studio operations in lower-cost countries like Latvia, Georgia, and Malta.

Operating Leverage & Scale: Once a studio is built, each new table and player adds revenue at a very high incremental margin. Its vast network allows it to serve thousands of operators from centralized production hubs, creating immense economies of scale.

Free Cash Flow & Capital Allocation: The business model is capital-light and generates enormous free cash flow, with a cash conversion rate often near 100%. Historically, capital allocation has been focused on:

Reinvestment: Modest organic CAPEX for new studios and games.

M&A: Acquiring RNG businesses to diversify.

Shareholder Returns: A growing dividend and, more recently, significant share buybacks.

4. Governance & Incentives

The company's founders retain 11% stake, while the largest shareholder is Kenneth Dart, owning 17% stake. CEO recently spent EUR6m to purchase 100,000 shares of Evolution AB, bringing his total ownership to 784,710 shares.

The Extra General Meeting on 9 November 2023 resolved to issue a maximum of 2,500,000 warrants. Each warrant entitles the holder to subscribe for one new share in the company for SEK 1,296.60 during the period from and including 16 November 2026 (however not earlier than the day after the publication of the company’s interim report for the period January–September 2026) up to and including the date that falls 14 calendar days thereafter. In total 1,995,389 warrants were subscribed. Given the share is currently trading at around SEK700 per share, it is likely that such warrants may expire next year worthless.

The annual general meeting in Evolution AB on 9 May 2025 resolved on an incentive programme under which the company invites approximately 250 employees within the group to acquire warrants in the company. Up to 2,050,000 warrants will be issued to the company or a wholly owned subsidiary and transferred to the participants of the incentive programme. Each warrant entitles the participant to subscribe for one new share, at a price equivalent to 130 per cent of the volume-weighted average price of the company’s share on Nasdaq Stockholm during a period from and including 2 May 2025 up to and including 8 May 2025. After a disappointing quarterly earnings announcement, the share price dropped by almost 20% on a single day, which could be good news for Evolution AB’s management team. It brings the share price to ~SEK670 during the 2-8 May period, therefore, the exercise price of the 2025-28 incentive plan is set to ~SEK870, a more achievable target that could incentivise the management team to act accordingly. I will explain later why this matters.

5. The Wall of Worry: Reasons for a Depressed Valuation

Despite its strengths, the stock trades at a valuation far below its historical average. This is due to a confluence of legitimate risks that have shifted the narrative:

Regulatory Headwinds: The trend of "ring-fencing" in European markets (where countries regulate and tax their online gaming markets separately) and the potential for a clampdown on its unregulated market exposure create uncertainty.

Margin Dilution: A necessary pivot to more heavily taxed and regulated markets will naturally pressure its industry-leading margins.

Slowing Growth: The post-COVID normalisation of online activity, coupled with execution issues such as cyberattacks, has slowed growth in the high-potential Asian market, bringing an end to its era of 40-50% growth.

Disappointing M&A: The expensive, dilutive acquisitions of RNG companies, such as NetEnt and Big Time Gaming, have, so far, failed to deliver the expected growth, raising concerns about the company's capital allocation prowess.

Slow US Progress: The state-by-state legalisation of iGaming in North America has been slower than many investors had hoped, tempering growth expectations.

6. The Contrarian View: A Compounding Machine in Disguise

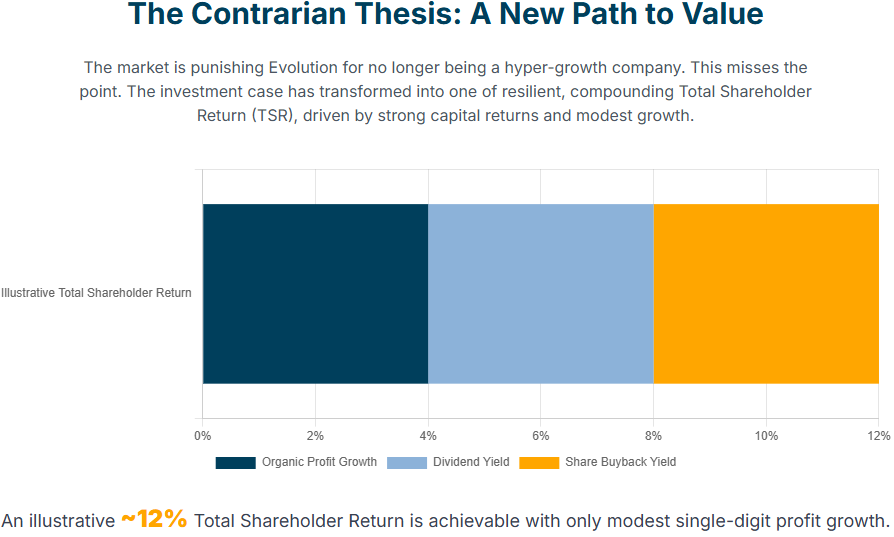

The market is punishing Evolution for no longer being a hyper-growth company. This misses the point. The investment case has transformed from one of explosive growth to one of resilient, compounding total shareholder return (TSR).

Consider this framework:

Shareholder Returns as a Baseline: With a net cash balance sheet and immense free cash flow, Evolution is now returning significant capital to shareholders. It currently offers a dividend yield of over 4% and has been buying back nearly 4% of its shares annually. This provides a powerful floor of ~8% return.

Modest Growth Delivers High Returns: The market is sceptical of a return to 20%+ growth. But Evolution doesn't need it. Suppose the company can achieve a modest, low-to-mid single-digit organic net profit growth of, for example, 4% per annum. In that case, the total shareholder return proposition becomes ~12% (4% growth + 8% capital return), assuming no change in P/E multiple. For a market leader with a deep moat, this is a highly attractive and achievable target that growth-oriented investors are likely to dismiss.

A Maturing Industry Can Be a Benefit: A maturing industry is less attractive to new entrants, reducing competitive threats. Furthermore, it often leads to consolidation. We have already seen evidence of this with Light & Wonder exiting the Live Casino space, ceding market share to dominant players like Evolution.

7. The Real Risk: The Curse of Too Much Cash

In my view, the most significant long-term risk to Evolution is not regulation or competition, but poor capital allocation—what I call "the curse of making too much money and not knowing what to do with it".

The company's biggest failure in recent years was the expensive, 17% dilutive acquisition of NetEnt. This strategic misstep, aimed at diversifying into the slower-growth RNG space, was masked by the phenomenal concurrent growth of the core Live Casino business.

While Evolution is the undisputed leader in its core vertical, history is littered with market leaders who lost focus through value-destructive M&A. If management gets distracted by empire-building instead of protecting and innovating within its core business, even a seemingly conservative 4% profit growth target could be missed. The discipline to either return its vast cash flow to shareholders or reinvest it at a very high rate of return is the single most important factor that will determine its long-term success.

While the risk of poor capital allocation can’t be avoided, the lower exercise price of warrants relating to the 2025-28 incentive plan may reduce the management’s incentive to take excessive risk. To realise any profit from the warrants, they only need the share price to be above ~SEK870 by May 2028, i.e. ~13x P/E based on EUR6 EPS or ~12x P/E based on EUR6.5 EPS. They don’t need 20% per annum EPS growth from EUR5.22 in FY2024 to make this happen. In hindsight, it was a brilliant move to take proactive and self-initiated actions to ring-fence regulated markets in Europe, which drove the share price down by 20% ahead of the Annual General Meeting.

Conclusion

I have built a small position in Evolution since April and increased my investment after the disappointing quarterly result announcement on 30 April. This article provides a summary of my analytical framework, and I will continue to publish articles offering more in-depth analysis on key debates often misunderstood by investors.

I also want to recommend a subscription to Ali Gündüz’s Substack, which provides excellent coverage of Evolution AB and helps me understand its risk/reward profile.

Thanks Bro, this is good stuff. Did management reflect on their acquisition of NetEnt? If this misstep (investor's perspective) is reflected and they would avoid going forward, this is actually positive. However, if management views the issue very differently than investor, there could be more value destructive M&A to come.

It's interesting to see the overlap in our portfolios. I initially came here for your excellent coverage of BAT and the broader nicotine space—thank you for that—but was pleasantly surprised to see you also cover Diageo (which is on my watchlist) and Evolution Gaming. I also initiated a position in Evolution this year for similar reasons, shortly after selling my stake in Philip Morris (too early).

One is tempted to say "great minds think alike," but it's more likely we're operating in a similar investment bubble. Let's hope it proves to be a profitable one!