Evolution Q2 2025: A Less-Feared Result Reinforces the Compounding Thesis

Evolution AB (STO: EVO) released its second-quarter 2025 results, and for investors who have weathered a volatile few months, the report was met with a palpable sense of relief. While the headline figures suggest a company treading water, the underlying operational narrative is one of methodical progress. The market reaction speaks volumes; the share price has rebounded over 20% from the trough recorded after the Q1 earnings release, suggesting these results were far less feared than anticipated.

Over time, as sell-side commentary more closely mirrors the reality Evolution is facing, my analysis will seem less counterintuitive and more like common sense. For now, let's examine how the quarter's performance reinforces the thesis that Evolution is transitioning from a growth darling into a resilient compounding machine.

Gauging True Momentum: The Game Rounds Index

To understand the health of Evolution's entire network, looking purely at revenue can be misleading. The RNG segment's growth of just 0.3% this quarter, for example, was heavily skewed by a record payout.

A far better measure of underlying customer engagement across both Live Casino and RNG is the Game Rounds Index. This metric, which tracks total player activity, grew a healthy 2.7% year-on-year and an even stronger 2.7% quarter-on-quarter (10.6% annualised). As the Q2 presentation shows on page 3, the index has followed a consistent, upward trajectory, separating the signal of genuine player engagement from the noise of short-term payout volatility. It tells us that more people are playing Evolution's games, which is the most fundamental driver of long-term value.

Geographical Performance: A Mixed Picture

The global story remains one of divergence, with challenges in Europe being offset by strength elsewhere:

1. Asia: Cautious Optimism as Cyberattack Countermeasures Take Hold

A key concern from the first quarter was the impact of "criminal cyber activity" in Asia, which pressured revenue growth. The CEO reported that the company is "starting to reap some benefits" from new technical countermeasures.

After posting €201.9 million in Q1, revenue from Asia grew 3.6% sequentially to €209.1 million in Q2. While the company remains "very cautiously optimistic," this sequential turn is a significant green shoot. However, it is worth noting that criminal cyber activity remains a persistent issue, and I don’t expect it to disappear overnight.

In a landmark move, Evolution launched its first-ever Asian studio in the Philippines during the quarter, marking a significant step into the first licensed iGaming jurisdiction in the region.

2. Europe: The Lingering Impact of Proactive Ring-Fencing

Challenges in Europe persisted. In Q1, Evolution took "proactive and self-initiated actions" to ring-fence certain regulated European markets to align with evolving regulatory standards. The company warned this would have a negative impact, and Q2 results show this playing out.

European revenues declined by 5.0% sequentially, falling from €189.7 million in Q1 to €180.2 million in Q2. Mr. Carlesund acknowledged that the financial impact may have been "larger than anticipated outside of the UK." This demonstrates the short-term cost of Evolution's strategy to stay ahead of the regulatory curve. While the company maintains that sensible regulation is ultimately beneficial, the European segment remains a drag on overall growth for now.

3. The U.S. Growth Engine: Firing on All Cylinders

North America remains a source of strength, with revenues growing 3.5% sequentially to €74.0 million. More importantly, Evolution made significant strategic moves during the quarter that bolster its long-term outlook in the region.

Key developments include:

Entering Rhode Island: An agreement with Bally's Corporation established Evolution's presence in all seven U.S. states that currently offer online casino gaming.

Expanded Hasbro Partnership: Evolution is now Hasbro's exclusive global provider for online casino games based on iconic brands like MONOPOLY. This includes developing new live casino and slot titles, reinforcing its entertainment-led approach.

Studio Expansion: The company is continuing to invest in capacity, with plans for a new studio in Grand Rapids, Michigan.

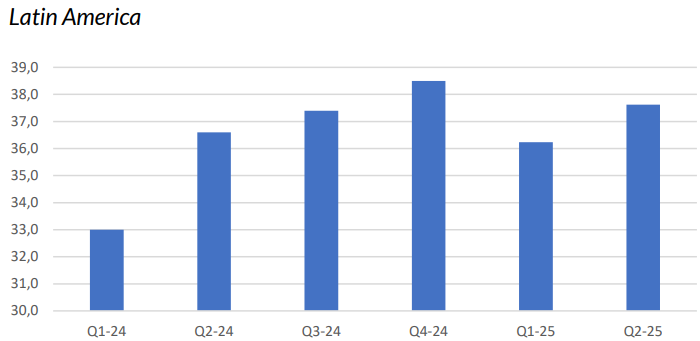

4. Latin America: Brazil Leads Expansion

Evolution's global expansion strategy is in full swing, with significant milestones achieved in key growth regions. The share of revenue from regulated markets stood at 44% in Q2, representing a significant increase from 39% in the same quarter a year prior.

In Brazil, timed with the country's transition to a regulated market, Evolution launched its new state-of-the-art studio in São Paulo after the quarter's end. Latin American revenue saw a healthy 3.9% sequential growth to €37.6 million, and the new studio is poised to accelerate this trend.

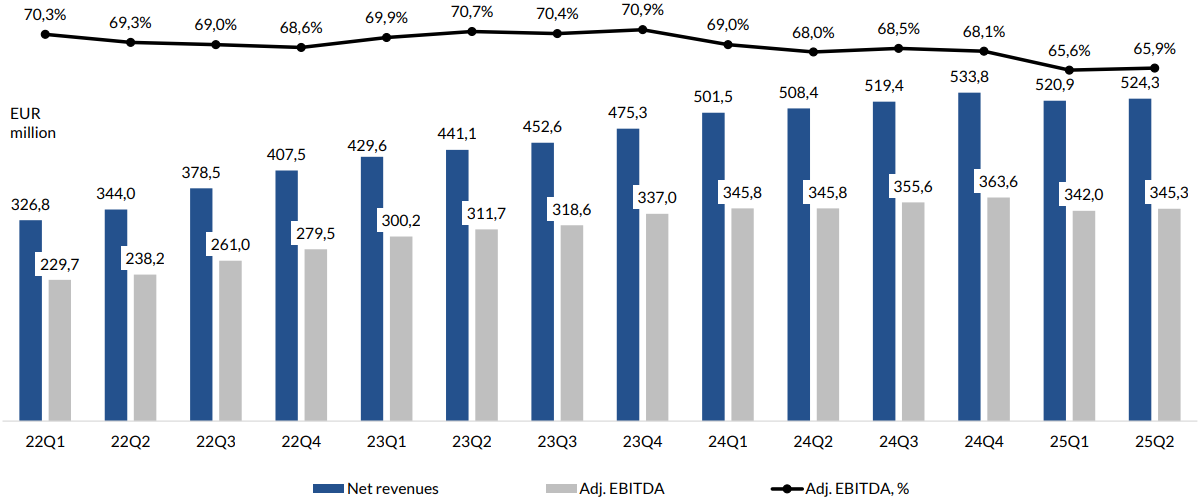

Profitability and a Clear Path to Guidance

The company reiterated its full-year EBITDA margin guidance of 66-68%. Far from being ambitious, this target appears well within reach. The H1 2025 margin was 65.8%, with Q2 coming in slightly higher at 65.9%. It is a stone's throw from the lower end of the range.

This guidance seems even more achievable when considering the phasing of investment. The company is incurring start-up costs for its new studios now, with the corresponding revenue set to ramp up in the coming quarters. This provides a natural tailwind that should help lift margins comfortably into the guided range in the second half of the year.

The reported profit for the period was also impacted by a -€11.9 million net financial loss, primarily due to FX movements. As a EUR-reporting company holding significant SEK cash for dividends and buybacks, the depreciation of the Krona during the quarter led to a valuation loss, a financial quirk rather than an operational flaw.

We Don't Need Another Hero: Why Mid-Single-Digit Growth is Enough

The key message from my previous article was that Evolution no longer needs heroic, double-digit growth to deliver compelling shareholder returns. The Q2 results provide concrete evidence for this thesis.

By annualising the sequential growth in operating profit (from €303.4m in Q1 to €306.4m in Q2), we arrive at an underlying growth rate of approximately 4%. This is the "mid-single-digit" growth that, when combined with an ~8% return from dividends and buybacks, is sufficient to generate a very attractive total shareholder return. Of course, with the share price increasing, returns from dividends and buybacks will diminish, requiring faster growth from underlying earnings to balance the equation.

Furthermore, the quality of this revenue is improving. The proactive ring-fencing in Europe, while painful in the short term, reduces the company's reliance on grey markets, de-risking the business and making that mid-single-digit growth more certain and sustainable over the long term.

Conclusion: A Renewed Focus on the Core

The most significant long-term risk for Evolution has always been the "curse of too much cash", leading to value-destructive M&A outside of its core expertise. The developments in Q2 offer reassuring evidence that this risk is being managed.

The core of Evolution's investment case has always been its dominance in Live Casino, a segment with high barriers to entry built on operational scale, technological expertise, and brand trust. This is the home ground Evolution cannot afford to lose, and Q2 results show it remains laser-focused.

Live Casino revenue grew 3.6% year-on-year to €453.7 million. This continued growth, even in the face of regional challenges, proves the resilience of the vertical. It is the engine of the business, and the company must remain focused on defending its moat here. As long as Evolution remains this focused, it will not only navigate the current challenges but will almost certainly exit this storm stronger than it entered. Quarterly earnings beat or miss will fade and be forgotten over time, while the quality of the business and the discipline of its capital allocation endure.

Nice write up - thanks for sharing.