Philip Morris Q2: Navigating Growth, Expectations, and Valuation

PM 0.00%↑

Yesterday, Philip Morris International (PMI) reported what was, by most objective measures, a very strong second quarter. Adjusted diluted EPS grew an exceptional 18.9% (ex-currency), the company raised its full-year guidance, and the smoke-free business continued its strong growth. The market’s reaction? A sharp 8.5% drop in the share price.

This response wasn't necessarily about a broken business, but rather a narrative getting ahead of itself. The share price movement, both the run-up before the announcement and the correction after, is justified when a stock is priced for perfection. This is the dynamic we'll explore.

For an overview of PMI’s Q2 2025 results, you may refer to the Tobacco Insider article for details.

The Perils of a "Beat-and-Raise" Mindset

It's natural to form a view on whether a company will beat or miss estimates. However, betting on a "beat-and-raise" quarter just before an announcement is a short-term, zero-sum game. By the time the results are out, those expectations are already priced in. When reality falls even slightly short of the most optimistic whispers, as it did with ZYN shipment volumes, the air comes out of the balloon fast.

Long-term investing is different. It is not a zero-sum game. It is the process of partnering with a solid business and allowing profits to compound over time, long after the excitement or disappointment from a single quarter fades. Yesterday's price action was a textbook example of the market's short-term voting machine operating with perfect logic based on the available information and pre-set expectations.

The ZYN Saga: Phasing, Not Faltering

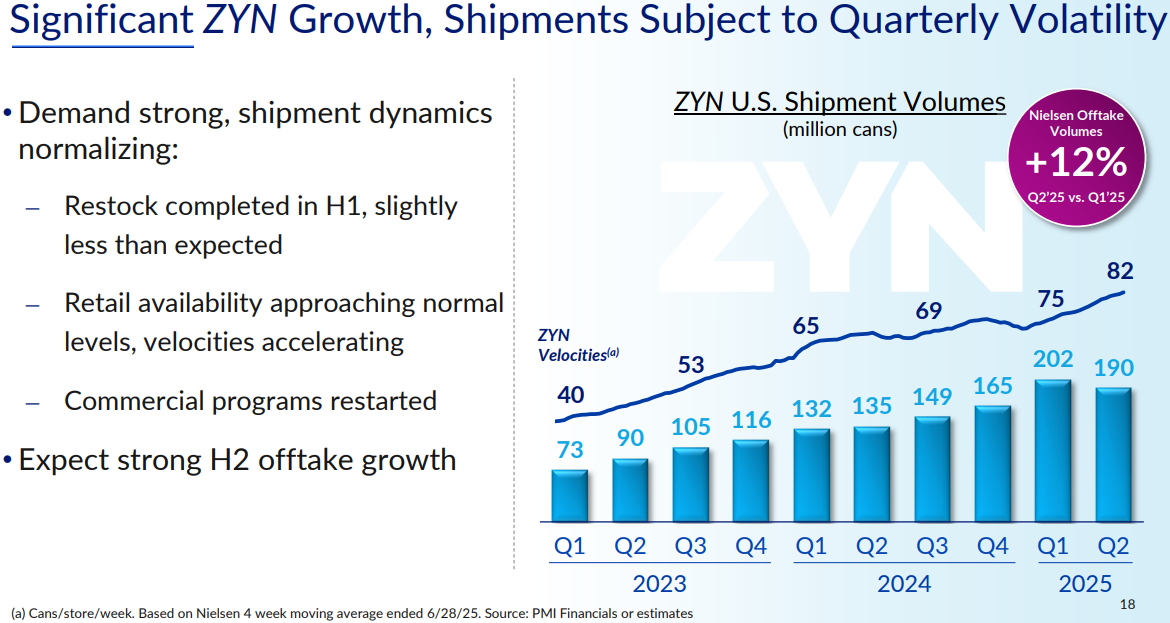

The primary source of anxiety was the sequential decline in ZYN U.S. shipment volumes, from 202 million cans in Q1 to 190 million in Q2. On the surface, this appears to be a slowdown. In reality, it was an expected and communicated dynamic.

As management guided in Q1, the first-quarter shipment number was artificially elevated by the significant restocking of wholesale and retail channels after a period of supply constraints. That restocking concluded in the second quarter. This is not a surprise; it's an accounting of inventory movements.

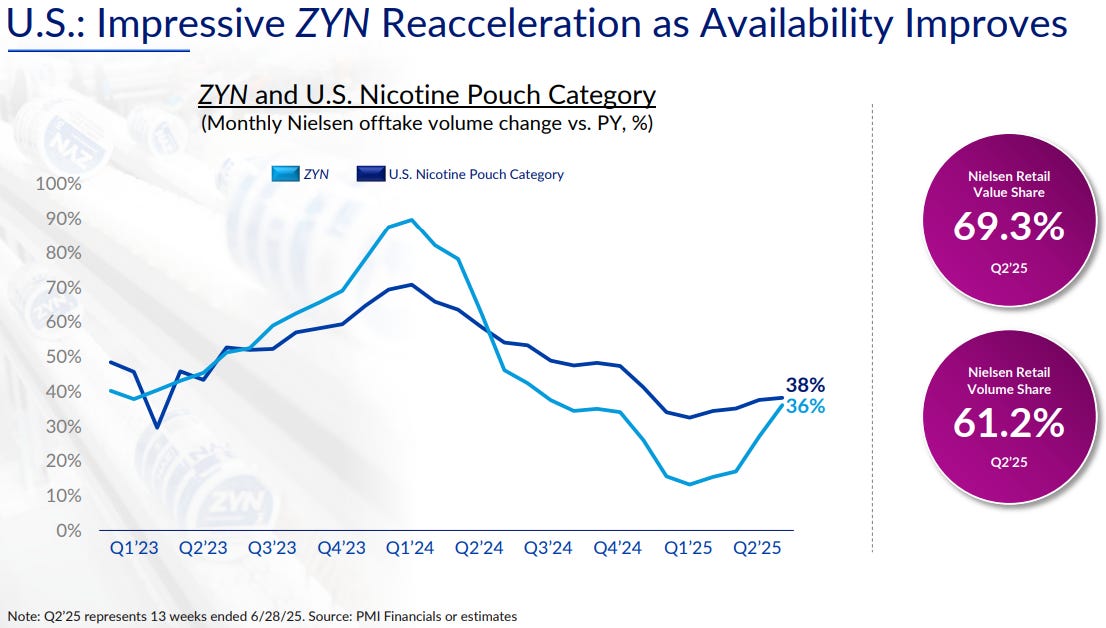

The more meaningful metric is retail off-take, which refers to what consumers are actually buying. Here, the story is one of strength. According to NielsenIQ data cited by management, ZYN’s offtake volume growth accelerated to ~37% year-over-year in the first two weeks of July. This represents a dramatic recovery from the ~15% growth seen in March, when shelves were empty, and it brings ZYN back in line with the overall nicotine pouch category's growth of ~39%. The most important metric, sequential market share, has been growing strongly since April.

As PMI highlighted in its earnings presentation, retail offtake sales velocity is also accelerating on a cans/store/week basis, which is similar to the same-store sales growth (“SSSG”) metric measured by the consumer retail industry. It is a strong testament to the brand's strength that ZYN is catching up to the category growth rate with minimal promotional and advertising investment, as its sales velocity grew from 75 to 82 between Q1 2025 and Q2 2025, extending a multi-year growth trend.

As I highlighted in my previous article on Q1 earnings, the real test begins now. With ZYN back in stock, its competitors, who relied on heavy promotions to gain share, are in a peculiar situation. Do they risk raising prices to sustainable levels now that ZYN is restarting its promotional spending? PMI is not the one in a tough spot; its competitors are.

The Elephant in the Room That No One Saw

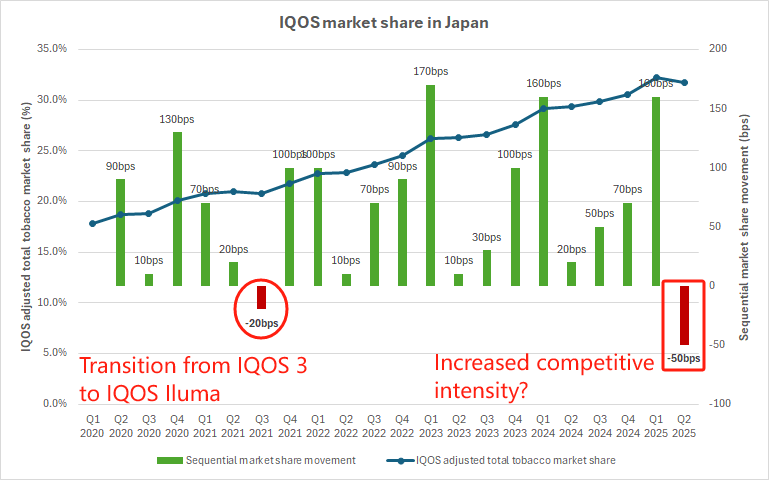

While Wall Street obsessed over ZYN, everyone missed a potentially more significant data point. In Japan, PMI's largest and most important IQOS market, heated tobacco unit (HTU) market share saw a sequential decline of 50 basis points, from 32.2% in Q1 to 31.7% in Q2.

This marks the first sequential decline in market share in Japan since the third quarter of 2021, when the company transitioned from IQOS 3 to the then-new IQOS ILUMA. The press release mentions "increased competitive intensity", but surprisingly, not a single analyst on the earnings call asked a follow-up question to understand what is driving this. I have read a few sell-side analyst reports before writing this article, but none discussed the 50bps sequential market share movement of IQOS in Japan. What is the impact of new competitor products like Ploom Aura and Glo Hilo? What is PMI's innovation pipeline to counter this?

Given that the success of IQOS is far more critical to PMI's global thesis than ZYN, this was a glaring omission. The market was so focused on the ZYN mouse that it missed the potential stirring of the IQOS elephant.

A Word on Valuation

The context for all of this is, of course, valuation. The sharp price correction is logical when you consider the premium at which PMI trades. PMI trades at a 2025E P/E multiple of ~22x (based on management guidance of $7.43 - $7.56 adjusted EPS excluding currency), which represents a significant premium to both its historical average (3-year historical average multiple of ~16x) and its tobacco peer group.

The market rightfully assigns this premium due to PMI's best-in-class growth algorithm, which consistently outpaces its peers in the tobacco and broader consumer packaged goods sectors. However, a premium valuation also means the stock is held to a higher standard. There is little room for error, and any data point that falls short of elevated expectations, even if strong in absolute terms, can trigger a swift de-rating, as we saw yesterday.

Key Strengths Overlooked in the ZYN Frenzy

Beyond the headline drama, several aspects of the quarter demonstrated prudent management and underlying business health:

Prudent Treasury Management: Some analysts questioned why the FX tailwind wasn't larger despite U.S. dollar weakness. Let's not forget that after a decade of the U.S. dollar strengthening, PMI has been actively hedging its exposure (e.g., in JPY) and shifting its debt to be more Euro-denominated. The goal isn't to maximise gains from currency swings; it's to manage risk and deliver predictable dollar-based profit growth, which they are doing successfully. During the earnings call, when questioned about the currency impact, CFO Emmanuel Babeau explained that the negative transactional impact from a volatile Swiss franc, where PMI has significant costs, "is to a large extent offsetting the benefit we have on the euro."

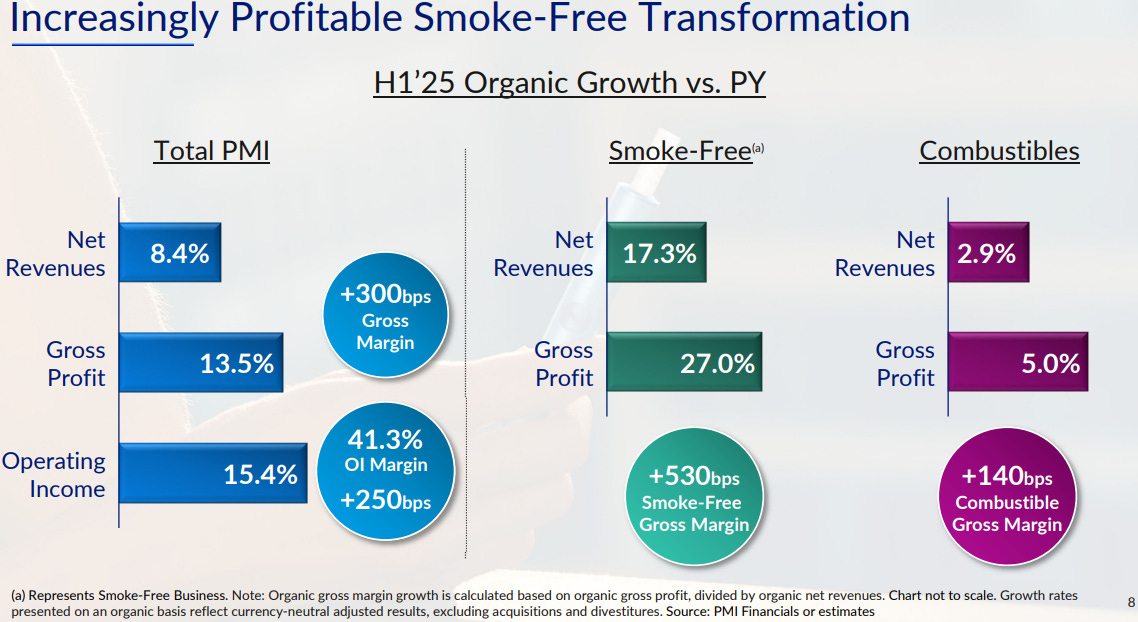

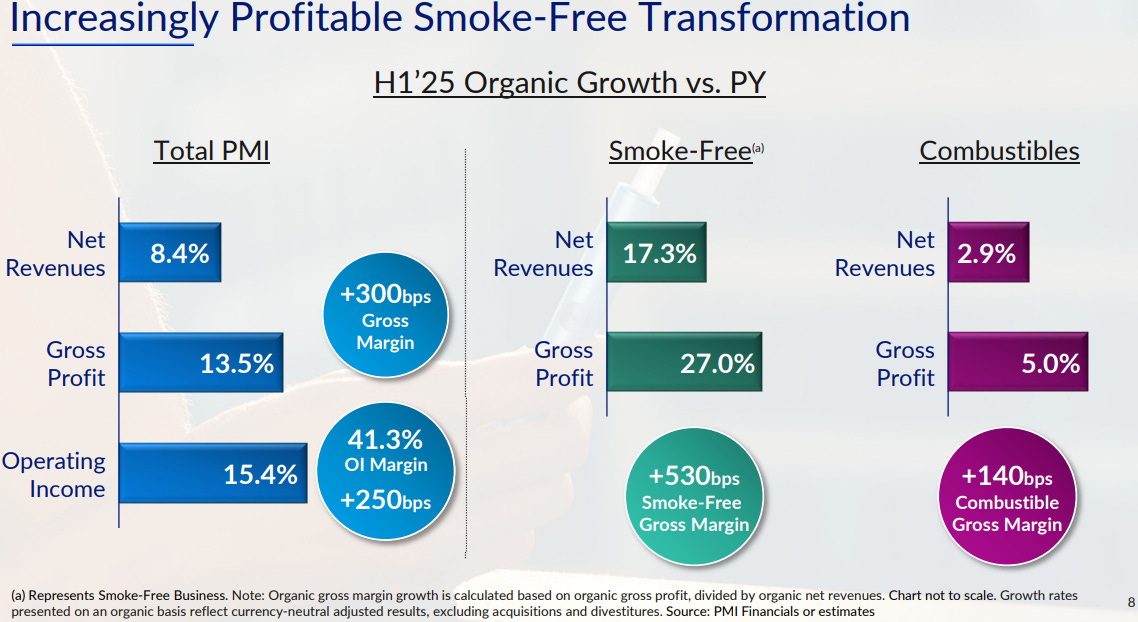

Strong Margin Performance: The narrowing gross margin gap between combustibles and smoke-free products was questioned. This performance was driven by both the smoke-free portfolio and a surprisingly robust combustible business, which saw its organic gross profit grow by 5.0% and deliver a 140bps gross margin expansion in the first half. As CFO Emmanuel Babeau noted, the improvement in combustible margins helped narrow the gap, a sign of strength, not weakness. If PMI can sustain its current smoke-free margins in the second half while reinvesting in ZYN, it would be a significant achievement, relying on IQOS's scale and the resilience of the combustible engine to balance the equation.

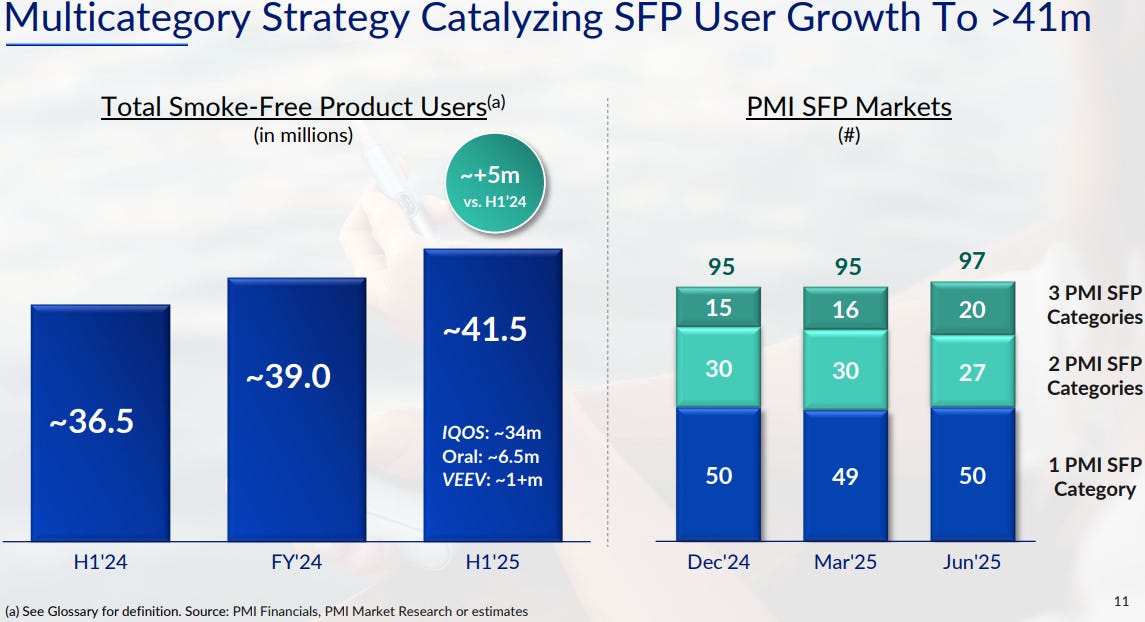

Source: PMI Q2 2025 earnings presentation The Quiet Rise of the Multi-Category: The strategic deployment of a multi-brand portfolio is accelerating. PMI now offers at least two of its smoke-free products in almost half of its 97 SFP markets, with the number of markets featuring all three brands (IQOS, ZYN, VEEV) jumping to 20 from 16 just last quarter. This strategy is designed to capture different consumer needs and usage occasions, accelerating the complete transition of adult smokers away from cigarettes.

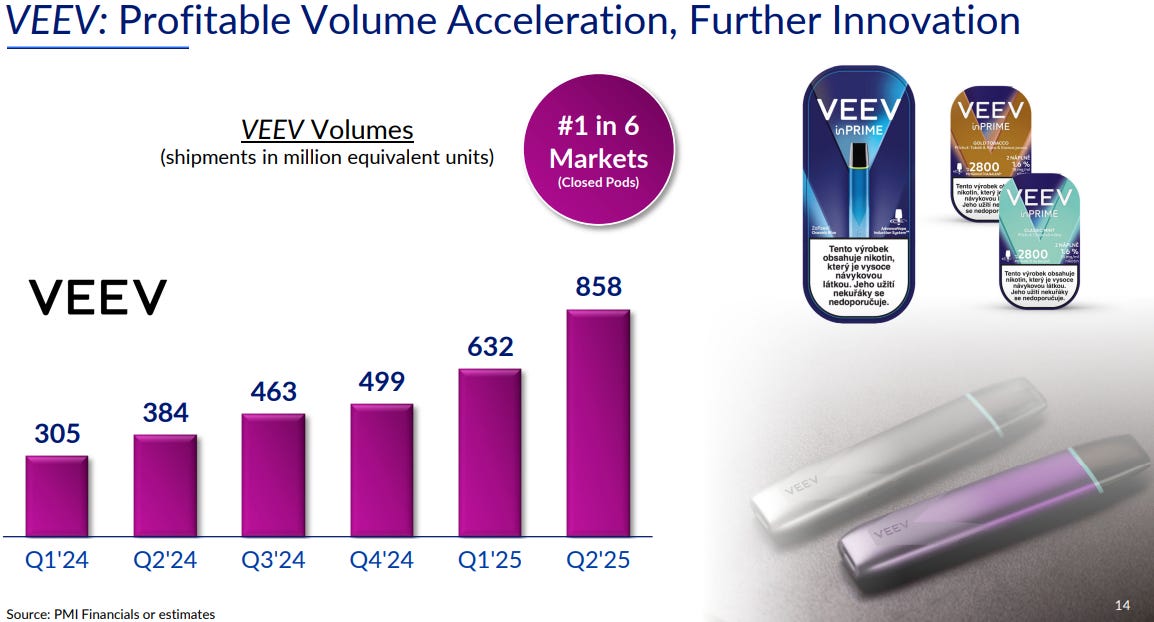

VEEV’s Profitable Acceleration: While still small, VEEV's progress is becoming material. Shipments more than doubled year-over-year, establishing it as the #1 closed-pod system in six European markets. More importantly, the business is becoming increasingly profitable. CFO Emmanuel Babeau revealed in the Q&A that VEEV's gross margin improved by "more than 10 percentage points" in early 2025 and that management believes it can achieve profitability "similar... as the combustible business." This demonstrates a clear path for VEEV to become a meaningful contributor, not just a drag on margins.

Source: PMI Q2 2025 earnings presentation

In conclusion, the market's reaction, while sharp, is understandable. When a stock with a premium valuation meets sky-high expectations, any perceived shortfall will trigger a correction. For long-term investors, the focus should now shift from the short-term noise of inventory movements to the long-term fundamentals. Regarding its smokefree portfolio, the most important thing is not the quarterly shipment number for ZYN, but the competitive landscape for IQOS in its most critical market.

Superb summary as always. My 2 cents.

1. PM is best in its class, but now priced for perfection. Who knows if and when we can expect its multiple to go back to 15x? Risk/reward is not what it used to be.

2. Times are changing.

Cigarettes are a unique business, superior to almost anything else. They offer high margins, low competition, loyal addicted customers, and no advertising.

Things will deteriorate with the growth of NGP. Nicotine will become just another FMCG category with lower margins and lots of competition.

The category will grow as nicotine is an awesome nootropic, and without cancer risk its popularity may be similar to what it was in the past. However, it will be a difficult business.

Any celebrity can launch a new pouch or vape brand, and I expect multiple new entrants.

Anthony, I've enjoyed your analysis of the tobacco/nicotine sector for quite some time. I consider you and and Invariant as my value-added commenters and opiners on this sector. You frequently unearth new content and are able to focus attention on what some short-sighted sell-siders sometimes dismiss or forget.