The Disaster Averted: Why BAT's "Overpriced" Reynolds Deal May Have Saved It from Itself

The 2017 acquisition of Reynolds American by British American Tobacco for $49.4 billion is a frequent topic of debate. Critics point to the high premium and the significant debt load BAT assumed, often concluding that the company overpaid. While the price was undeniably steep, this perspective misses a crucial counterfactual: What would have happened if the deal had fallen through?

In an alternate universe without the Reynolds acquisition, BAT, flush with strong free cash flow and borrowing power, could have made far more value-destructive decisions. The Reynolds deal, in hindsight, forced capital discipline by preempting far riskier bets, protecting BAT from the siren songs of an era defined by cheap money and speculative fervour.

To understand why, we must first revisit the business environment of 2017.

Setting the Scene: The Five Forces of 2017

Five powerful forces were converging, creating a perilous landscape for a company like BAT had it been looking to deploy billions in capital:

The Zero-Interest Rate Policy (ZIRP) Environment: In 2017, the world was awash in cheap money. The US Federal Reserve’s key interest rate was beginning to climb from near-zero, sitting at a mere 1.25-1.50% by year-end. In Europe, rates were even lower. This environment encouraged companies to increase leverage and pursue growth, sometimes at any cost.

The Cannabis “Gold Rush”: The legalisation of cannabis in Canada (2018) and a growing number of U.S. states created a speculative bubble of epic proportions. For Big Tobacco, cannabis seemed a logical “beyond nicotine” strategy, given the parallels in agriculture, regulation, and distribution. Valuations soared to unsustainable levels, driven by hype rather than fundamentals.

The IQOS “Fear of Missing Out”: Philip Morris International’s (PMI) IQOS was a runaway success, proving that a heat-not-burn product could genuinely disrupt the cigarette market. This success created immense pressure on competitors. As the valuation gap between the forward-looking PMI and the seemingly legacy-bound BAT widened, the “fear of missing out” would have driven an urgent, and potentially reckless, search for a competitive response.

The ESG Tsunami: The years 2017-2018 marked a pivotal turning point for ESG (Environmental, Social, and Governance) investing. According to data from Calastone, the global funds network, investor appetite for ESG funds exploded in the autumn of 2017. Between August 2017 and April 2020, net inflows into ESG funds were 37 times greater than in the preceding three years. This wave of ESG-driven fund flows forced asset managers to adopt strict no-tobacco policies, crushing tobacco stock valuations regardless of their underlying cash flow generation.

The Credit Rating Imperative: As ESG pressure mounted, credit rating agencies began placing greater emphasis on the growth and profitability of Next Generation Product (NGP) portfolios. A robust NGP strategy was seen as credit-positive, signalling a sustainable future for cash flows and debt servicing. This created a powerful incentive for tobacco companies to be seen as investing heavily in NGPs, even if the path to profitability was unclear.

The Financial Scorecard: Analysing the Path Taken

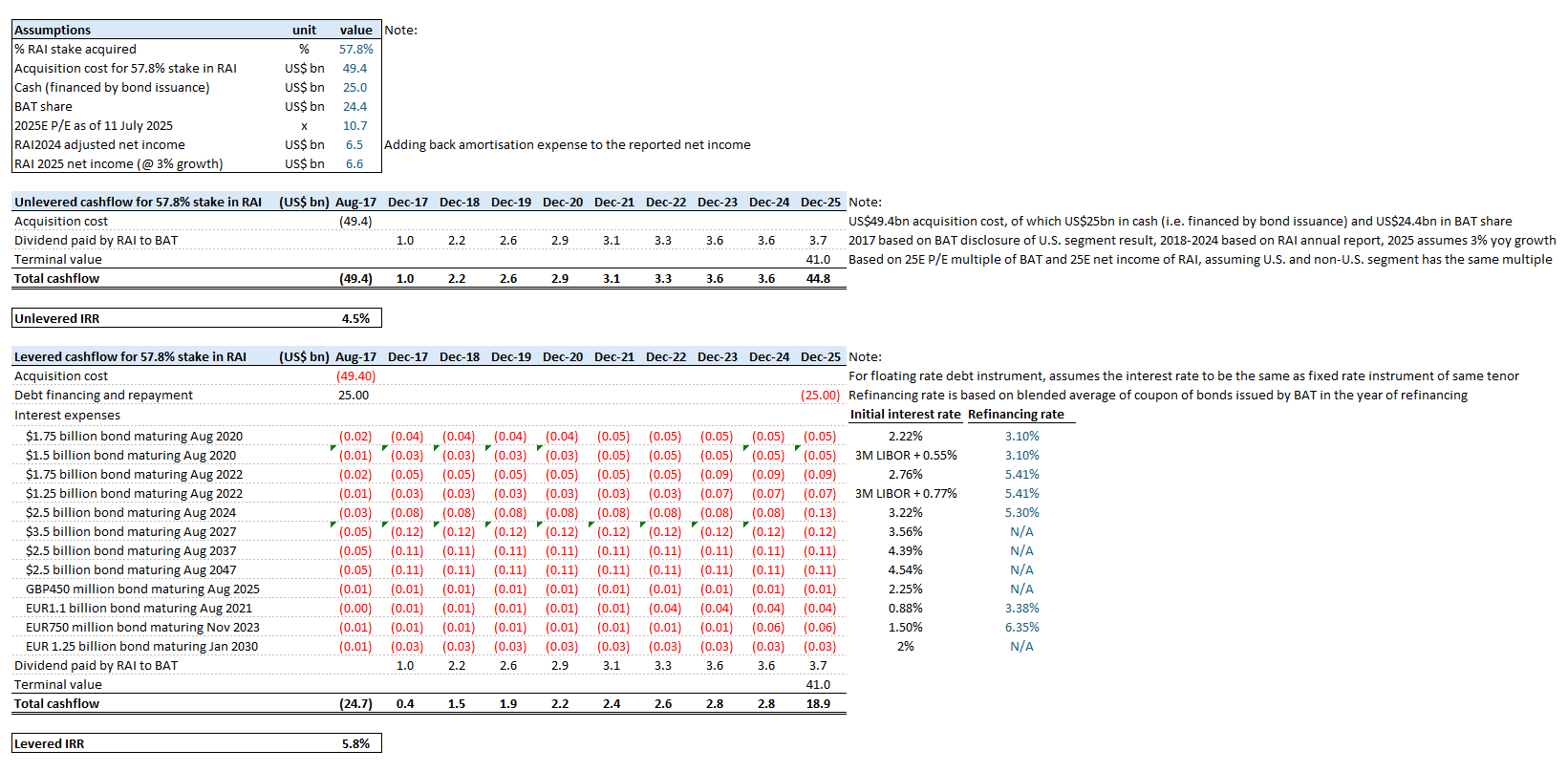

Given this backdrop, let's first evaluate the deal that actually happened. Critics are right about one thing: on a standalone basis, the Reynolds deal was no bargain. My analysis, running from the 2017 acquisition to a hypothetical exit in 2025 (though one may argue it is still early to tell), reveals a sobering financial verdict: unlevered IRR of 4.5% and levered IRR of 5.8%. It confirms the deal was not value-accretive on its own merits. But to judge it fairly, we must compare it not to perfection, but to the likely alternatives.

The Alternate Universe: A Landscape of Temptation and Prudence

Now, let's step into the alternate universe where the Reynolds deal fell through. With immense pressure to act, BAT would have faced a landscape of tempting, but treacherous, opportunities.

Path 1: The Value-Destructive Traps

The most likely paths would have been chasing the fashionable investment themes of the day.

The Vape Trap

Without Reynolds’ Vuse brand, BAT would have been desperate to acquire a leading vape asset. The likely targets would have been a minefield:

Juul: BAT could have preempted Altria’s disastrous $12.8 billion investment, which was subsequently written down to almost zero.

NJOY: Another Altria acquisition, this one for $2.75 billion, which was almost immediately hobbled by an FDA import ban on its key products.

RELX: Acquiring a leading Chinese vaping company would have exposed BAT to immense regulatory and geopolitical risk, which has since crippled the industry in China.

Heaven Gifts (Elf Bar/Geek Bar): While commercially successful, these brands have operated in a regulatory grey area. An acquisition by a compliance-focused multinational like BAT would have been a culture clash, likely stifling the very agility that made them successful. Let’s imagine if BAT had acquired Heaven Gifts before Elf Bar was banned in the U.S. While one may argue that Heaven Gifts is a resilient business that has managed to recapture the market through its majority-controlled Qisitech and launched Geek Bar in place of Elf Bar, BAT may not be equally flexible and agile in making such a move as a public company. The management team at Heaven Gifts might lack the incentive to pursue the “Qisitech route” as they didn’t own the business anymore. Why bother to take a risk for BAT’s benefit? They could leave Heaven Gifts and start anew at Qisitech or elsewhere, following the ban on Elf Bar.

The Cannabis “High” and Subsequent Crash

This represents another likely path to catastrophic value destruction other than the vape trap. With a strong balance sheet and a mandate to pursue “beyond nicotine” growth, BAT would have been under immense pressure to make a significant play in cannabis. The cautionary tales were yet to be written:

Constellation Brands invested over $4 billion into Canopy Growth, an investment that has since lost the vast majority of its value.

Altria wrote off almost the entirety of its $1.8 billion investment in Cronos Group.

It is highly probable that in this alternate universe, BAT would have made a similarly significant and ill-timed investment at the peak of the cannabis bubble, destroying billions in shareholder value.

Path 2: The Roads Not Taken

There were, of course, more prudent options. However, these were strategically and culturally untenable.

The "Sinful" Stigma of Combustibles: The most logical and profitable use of capital might have been acquiring smaller, cash-generative cigarette companies to consolidate market position or enter new markets. However, in the ESG-obsessed environment of 2017-2019, this would have been a thankless task. Management would face immense pushback from the board and investors for doubling down on a “dying” industry. Any failure in an NGP acquisition was forgivable as “investing in the future”; a minor misstep in a combustibles deal would have been a career-ending mistake. After all, the combustible segment is not without its own legal and compliance risk.

The "Passive" Share Buyback: The most financially disciplined path was a sustained share buyback, offering a stable ~6.5% earnings yield. But this would have been seen as an admission of defeat. It wouldn't solve the US market problem or the NGP arms race, and it ran contrary to a corporate culture geared for bold, expansive action.

Conclusion: The Best Deal Was the One That Tied Their Hands

This brings us to the final verdict. When we compare the financial outcome of the path taken against the most probable alternate paths, the picture changes dramatically.

The Reynolds acquisition generated a positive, albeit low, Levered IRR of 5.8%.

The likely alternatives offered catastrophic returns:

The potential IRR of acquiring Juul: Effectively -100%.

The potential IRR of investing in Canopy Growth: Approaching -90% or worse.

The acquisition of Reynolds American, while expensive, achieved something crucial: it imposed capital discipline. It absorbed BAT’s financial capacity, preventing management from chasing the disastrous investment trends of the era. Instead of a speculative cannabis play or a write-down-in-waiting vape acquisition, BAT secured a portfolio of highly profitable brands and a world-class NGP platform in Vuse.

The deal anchored BAT in the reality of cash flow, not the fantasy of hype. Sometimes, the most strategic move is the one that limits your options, protecting you from the market's most seductive and dangerous temptations.

Not much trust in the management; believing the best course of action is to tie their hands.

But it's so true. Having too much cash is usually a dangerous place to be in, leading to waste and stupid decisions.

This was really an interesting take on the acquisition, thanks for sharing your thoughts!

I don't agree, though, with this point: "This wave of ESG-driven fund flows forced asset managers to adopt strict no-tobacco policies, crushing tobacco stock valuations regardless of their underlying cash flow generation."

The share prices of big tobacco were riding all-time-highs in 2017 and early 2018. Hence, BAT's acquistion of Reynold's America proved to be particularly ill-timed.