BAT - 1H 2025 pre-close trading update

BAT provided a 1H 2025 pre-close trading update yesterday. Revenue guidance for FY25 was increased from 1% to 1-2%, while adjusted profit from operation guidance remained unchanged at 1.5%-2.5%. This is primarily driven by better-than-expected U.S. cigarette performance, strong Velo Plus performance in the U.S. and Velo in the international market, partially offset by poor U.S. vaping performance due to the proliferation of illicit disposable vapes. Overall, there’s not much surprise. For a detailed overview of the trading update and conference call, please refer to this Tobacco Insider article.

BAT share price increased by 1.4% yesterday, versus a flattish FTSE100 index. I don’t know if there’s anything worth cheering. In this article, I want to do a deep dive into the following issues:

What drives the recovery of BAT’s U.S. cigarette category? Is it cyclical or structural?

How shall we look at the revival of BAT’s U.S. modern oral category?

Will Glo Hilo's launch in key markets in 2H 2025 reverse the multi-year decline in market share in the heated tobacco category?

Mid-teens revenue decline of VUSE - What happened? So what? What next?

How shall we see the NGP / smokefree portfolio as a whole?

U.S. cigarette category

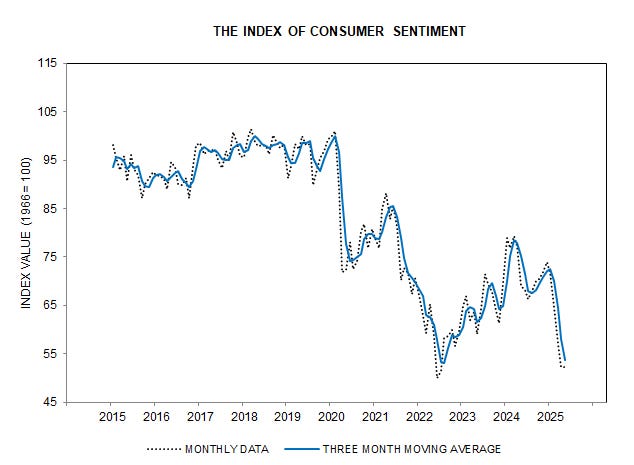

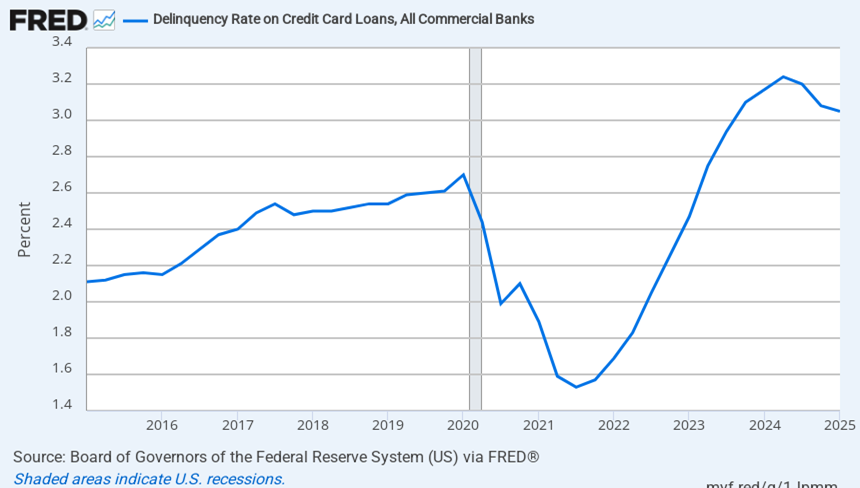

U.S. consumers remain under pressure due to accumulated inflation and a prolonged high-interest-rate environment, resulting in weak consumer confidence and a high credit card delinquency ratio. This has prompted consumers to downtrade from premium cigarettes to deep-discount cigarettes. Due to the proliferation of illicit disposable vapes and the rapid growth of the modern oral category, cross-category movement adds to the pressure of volume decline.

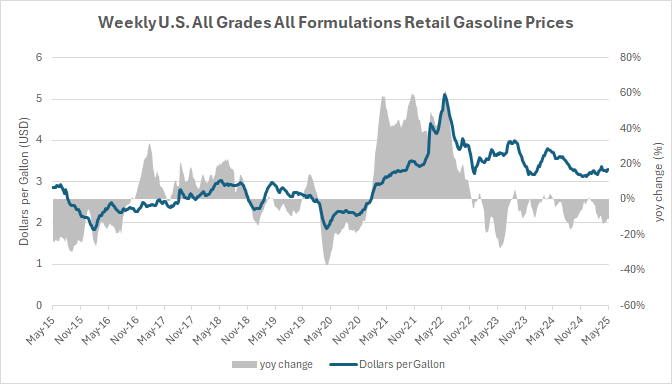

On the other hand, cigarette consumption has historically been negatively correlated with gasoline prices. We are seeing a moderation in gasoline prices, although they remain significantly higher than the pre-COVID levels. Still, it has a positive impact on cigarette consumption, alleviating the pressure of volume decline (though the downtrading trend continues).

What remains to be seen is the impact of the tariff on U.S. consumer behaviour. This will take time to unfold.

At a company-specific level, BAT has tried to right the ship by identifying and focusing on the controllables:

Price laddering of Newport by launching a “soft pack” version, which is slightly cheaper than the standard version, to address the downtrading concern.

10% increase in sales representative headcount in the U.S. to support increased retail outlet contract coverage from 82% in Q3 2023 to 88% in Q4 2024.

More competitive pricing, supported by direct-to-consumer rewards, investment in data analytics and revenue growth management, enabling differentiated pricing across regions.

Strong market share growth of Natural American Spirit in the premium segment and Lucky Strike in the branded discount segment.

All considered, the cross-category movement due to the proliferation of illicit disposable vapes remains a structural headwind that will persist until the U.S. government steps up enforcement against it, and the FDA will need to expedite the PMTA approval of flavoured pod-based vaping. We haven't seen any game-changing moves by the FDA thus far, though the new leadership may eventually implement changes. Downtrading to a deep discount category is more likely to be a cyclical issue, which may reverse once the impact of accumulated inflation fades and interest rates decline, assuming U.S. inflation remains stable.

Velo Plus and the U.S. modern oral category

BAT is delivering encouraging results in the U.S., driven by Velo Plus, with strong trial and retention rates driving total volume share of Modern Oral +550bps to 11.9% and triple-digit revenue growth. The statement above refers to BAT’s 1H 2025. Does it sound familiar to you? Let’s look at the comment and financials extracted from BAT’s 1H 2021 results.

In Modern Oral, Velo revenue increased 17% in the first six months of 2021 (to £8 million), or 29% at constant rates of exchange, as the Group invested in consumer acquisition and geographic expansion, with volume up 450%. Following the acquisition (in October 2020) of the nicotine pouch products from Dryft, the expanded range of products is now present in approximately 80,000 stores under the Velo brand and we will continue to build distribution further. Velo volume share has increased by 840 bps from FY 2020 to reach 16.0% May YTD 2021 in a competitive market.

What has happened since then? Let’s look at the FY2021 full-year results. While the first half produced GBP8m revenue on 405 million pouches volume (i.e. GBP0.4 revenue per 20-pouch can), the second half produced negative GBP6m revenue on 197 million pouches volume (i.e. negative GBP0.6 revenue per 20-pouch can).

In Modern Oral volume was up 272% with reported revenue down 82% (2021: £2 million; 2020: £10 million) in a highly competitive market, as the Group invested in promotional pricing and the national roll-out of the Velo branded nicotine pouch products. The expanded range of products is now available in over 110,000 stores under the Velo brand. Velo volume share increased 410 bps from 2020 to reach 11.7% in December. While growing year on year, driven by distribution expansion by the Group and other industry participants, the Modern Oral segment remains small, only representing around 1.6% of total nicotine value share. Low levels of average daily consumption due to high levels of poly-usage with other nicotine categories supports the Group’s multi-category approach.

While it is relatively uncommon, revenue can be negative in extreme cases, as seen in the example mentioned above. To BAT, negative GBP6m revenue can easily be lost in the rounding, so it doesn’t make sense for them to elaborate on the fact that “the Group invested in promotional pricing”. To understand this, we will have to look at BAT’s accounting policies as found in its annual report.

Revenue principally comprises sales of cigarettes, other tobacco products, and nicotine products, to external customers. Revenue excludes duty, excise and other taxes related to sales in the period and is stated after deducting rebates, returns and other similar discounts and payments to direct and indirect customers.

In other words, if the aggregate amount of rebates, returns and other similar discounts and payments to direct and indirect customers exceeds the after-tax sales, then revenue can be negative. To put it in perspective, let’s compare the NielsenIQ retail sales data versus the reported financials by BAT in 2021 concerning Velo. Remember that BAT don’t sell its products to consumers directly. BAT first ships its products to wholesalers, such as Performance Food Group (NYSE: PFGC) and McLane Company (owned by Berkshire Hathaway). These wholesalers then distribute the products to convenience stores and gas stations for sale to consumers. When volume growth reported by BAT vastly exceeds retail sales growth, it raises a red flag, indicating a risk of sales decline.

Furthermore, to conduct a national roll-out of a product that lacks competitiveness, it involves heavy subsidies to wholesalers and retailers in the form of “rebates and promotional incentives”. You may find a detailed description below, which I extracted from Performance Food Group’s annual report.

We participate in various rebate and promotional incentives with our suppliers, either unilaterally or in combination with purchasing cooperatives and other procurement partners, that consist primarily of volume and growth rebates, annual and multi-year incentives, and promotional programs.

To put the above-mentioned in perspective, even if BAT is willing to offer its products to consumers for free, its network of wholesalers and retailers won’t do it for free and needs to charge a certain margin. Let’s suppose selling a can of ZYN at a US$1 profit margin for the retailer (not unreasonable, given the average sales price of US$5.36 in December 2021) and VELO sources its customers from ZYN. Why should a retailer seek less than a US$1 profit margin from selling VELO?

I am not suggesting that the tragedy in 2021 will repeat in 2025, as Velo Plus appears to be a more competitive product, based on user feedback. Still, it will take time to observe its market share momentum after BAT reduces promotional investment and increases pricing. Retailers don’t care whether the market leader is ZYN, On! or Velo Plus, as long as they can earn the profit margin that they are entitled to.

Glo Hilo launch and the heated tobacco category

Glo’s volume share in top markets -90bps, driven by a highly competitive environment in Japan and the continued phase-out of legacy, super-slims platform. AME volume share -10bps, with continued share growth in Poland, Czech Republic and Spain, and a stable share performance in Italy, offset by competitive dynamics in Germany and Romania. I think we can conclude that Glo Hyper Pro doesn’t live up to its expectations. The legacy platform is believed to be in collaboration with BYD Electronic (285. HK), and it will be phased out gradually. All eyes are on Glo Hilo, BAT’s latest heated tobacco platform in cooperation with Smoore International (6969.hk).

As I mentioned in my previous article, Glo Hilo pilot launch in Miyagi Prefecture (宮城県), Glo Hilo will be available in Miyagi Prefecture (宮城県) starting from 9th June. We will need to see the market share data several quarters after the nationwide launch to assess its performance. Even for IQOS Iluma, it took around three quarters since its initial launch for the market share to show a meaningful change.

To add a bit more colour to it, I would like to share an expert interview article (with someone working at Smoore International) with you, which was first posted by a user on Xueqiu. The article is in Chinese, but you may use the auto-translate function of your web browser to read in English.

The feedback from the expert is consistent with my previous article, Smoore & Glo Hilo - Taking 10 Years to Sharpen a Sword (十年磨一劍). While only Japanese consumers can tell whether Glo Hilo is a good product, we know for sure BAT has licensed the proprietary processing technology IP owned by Smoore (i.e., how tobacco leaves are processed to form tobacco sheets for heating) with an ongoing royalty payment/profit-sharing arrangement linked to shipment volume. If Glo Hilo becomes a successful product, Smoore may then license its heated tobacco technology to other tobacco companies, for example, China National Tobacco Corporation.

BAT currently only takes care of manufacturing, marketing, and branding, as well as legal compliance, while leaving R&D, sales, and distribution to third parties. Since BAT doesn’t own the core IP to the Glo Hilo platform, even if it manages to gain market share in Japan and Italy, over the long run, it could be a costly victory with low reward. Think about the potential competitions and profit sharing by Smoore.

Vuse and the vapour category

Vuse’s global value share in top markets flat, with continued global leadership in tracked channels. Expect mid-teens revenue decline in H1, mostly driven by illicit Vapour headwinds in U.S. and Canada.

As the proliferation of illicit disposable vapes continues in the U.S., Vuse’s largest market, everything else doesn’t matter. When the legal market is shrinking, there’s not much within BAT’s control to rectify the situation. As I have mentioned many times, we must face the reality that enforcement will never be entirely effective. As the former head of research at General Motors, Charles Kettering once said, “A problem well-stated is half-solved”. If the U.S. government continues to believe that the black market in the U.S. is driven by the influx of disposable vapes from China, then it will remain a persistent problem. In light of the U.S. regulatory environment and trade policies, many Chinese e-cigarette manufacturers have established a manufacturing footprint in Southeast Asia. I would refer to the following article for more details.

Geekvape Unveils New Indonesian Factory: Revisiting Relocation of China's Vape Supply Chain

Qisitech, the company behind Geekvape, opened a new factory in Indonesia in 2023, creating more than 1,000 local jobs. While it takes years for the U.S. FDA and other government agencies to approve the legal product, tighten state legislations and step up enforcement, it only takes months or even weeks for Qisitech to relocate machinery and find a new shipping route. Who is to be blamed for creating this USD7bn black market and trade deficit?

While BAT also mentioned “Improving H2 revenue performance, driven by the phased roll-out of our new premium Vapour product, Vuse Ultra, and continued targeted resource allocation”, so far I haven’t seen any traction in Canada yet, where Vuse Ultra was launched in April 2025.

For investors tracking the performance of Vuse based on NielsenIQ data, I also want to highlight the fact that retail sales fell short of shipments from BAT in FY2024, indicating potential retail inventory de-stocking in FY2025. My estimate would be around 10% impact on volume in FY2025 if the excess retail channel inventory were entirely unwound.

NGP / smokefree portfolio

BAT mentioned that “We expect low-single digit New Category revenue growth in H1, accelerating to mid-single digit for FY. Excluding the impact of the U.S. and Canada Vapour markets, we expect double-digit New Category revenue growth for FY.” Whenever there’s any weakness in specific categories or geographies, BAT’s narrative has always been consistent. It is operating a multi-category business across multiple geographies. Investors can’t expect BAT to fire on all cylinders, but we shall expect stability of the overall Group performance.

While I agree with the above, I also want to add that what makes the NGP / smokefree portfolio very different from its combustible business is that the NGP / smokefree category is always subject to higher capex intensity, heavier R&D investment and sales & marketing expenses due to the continuous evolution of product formats and consumer preferences. Glo Hyper was once successful in 2020-2021, but what’s next? Vuse was growing nicely in 2021-2023, but what’s next? Velo picked up the torch in 2024-2025, but what’s next? It is a never-ending story.

In some cases, the regulatory environment is to be blamed. If we take a step back, a lack of commitment and urgency can be equally, if not more, damaging. While a multi-category approach offers diversification benefits, it also compromises accountability in case of failure. Being fully committed to a competitive category may risk failure, but adopting an experimental approach almost guarantees it. The inability of the Glo Hyper platform is a good example illustrating that. BAT simply moves on to its next experiment, Glo Hilo.

It is worth noting that while BAT raised its revenue guidance for the full year, the additional revenue doesn’t flow to the bottom line, as it decides to deploy the extra revenue for product rollout in 2H 2025, such as Velo Plus (expansion of retail outlet penetration from 110,000 to 130,000 in the U.S.), Glo Hilo (launch in Japan and other key markets in Europe) and Vuse Ultra. Let’s be patient and see how that unfolds.

As usual, there’s no buy/hold/sell recommendation or target price in my article, but you may find everything else you need to take away from BAT’s pre-close trading update. Hope you enjoy reading!

You're on track to becoming the best tobacco analyst who freely shares his ideas on the Internet.

It is now clear that traditional cigarettes and Next Generation Products (NGP) represent fundamentally different business categories. While traditional cigarettes are the best business to be in, pouches and e-cigarettes are poised to become highly competitive commodities, a trend amplified by celebrities launching their own brands.

Only IQOS, differentiates itself through its adoption of the 'razor and razorblade' business model.