I just attended the FY24 results presentation of Smoore International, and interestingly, ALL questions raised by research analysts are related to the launch of Glo Hilo, BAT’s latest HNB product. Smoore International confirmed its role as a key supplier to Glo Hilo, providing a total solution to the product’s R&D, which I alluded to earlier in the article Glo Hyper Pro product launch. The CEO of Smoore used the Chinese phrase “十年磨一劍” to summarise the product launch, which literally means “it takes 10 years to sharpen a sword”. Smoore started researching and developing heat-not-burn technology in 2014 but only launched the first product in 2024 with BAT. More specifically, it took 4 years for Smoore to co-develop Glo Hilo with BAT, leveraging its technology IP and manufacturing know-how accumulated over many years.

Note: the lady highlighted in red is Ms. Eve Wang, who is responsible for the strategic planning of Smoore and collaboration with ODM customers. She also appeared in BAT’s 2024 Capital Markets Day video.

Here are Smoore’s comments on the product. As usual, I hope this article provides insights and information rarely covered by mainstream sell-side analysts. Here we go!

The pilot launch in Serbia has been very successful and exceeded both BAT’s and Smoore’s expectations. Feedback from consumers shows that the product excels in three areas, differentiating it from IQOS Iluma, the leading product in the market.

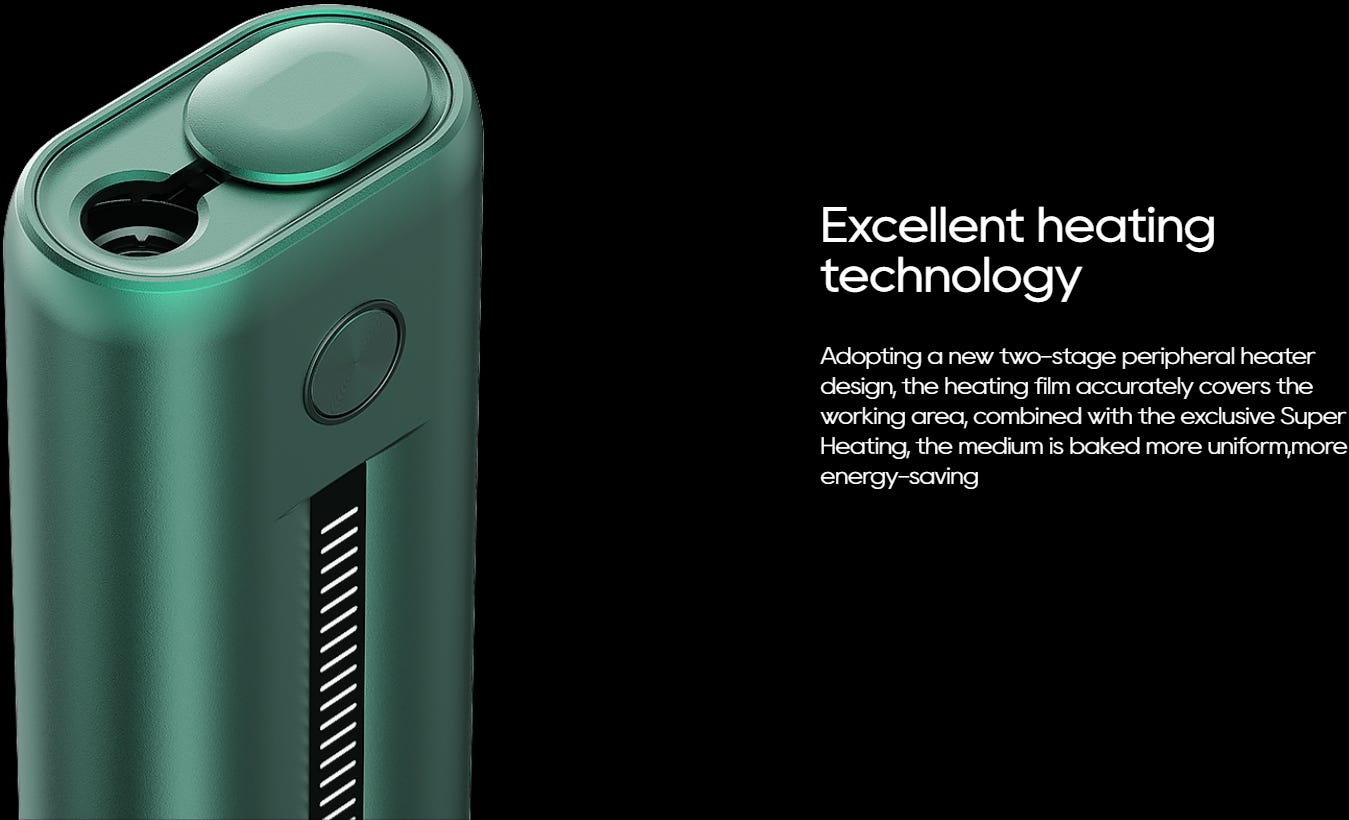

Smoore’s advanced heating technology shortens the pre-heating time of tobacco sticks to 5 seconds, compared to the 20 seconds required by IQOS Iluma. This significantly upgrades the user experience and could meaningfully change users’ behaviour, which leads to more effective conversion of cigarette smokers. (note: For cigarette smokers, convenience is essential, and it shouldn’t take 20 seconds to light a cigarette. So why should they wait for 20 seconds to pre-heat a heated tobacco product? It is a pain point that IQOS has not yet addressed.)

Smoore also redesigned the processed tobacco sheets, while BAT still manufactures them in its existing facilities. BAT has licensed the proprietary processing technology IP owned by Smoore (i.e., how tobacco leaves are processed to form tobacco sheets for heating) with an ongoing royalty payment/profit-sharing arrangement linked to shipment volume. The latest processing technology allows maximum taste and aroma release to restore conventional cigarettes' taste. This is particularly relevant to converting heavy smokers who desire an authentic taste of tobacco.

EasyView LED screen and beautiful industrial design position Glo Hilo as a premium platform.

Smoore recognises that consumers in different markets have a wide array of preferences. Hence, it will adjust the product accordingly to support BAT’s global launch in 2H 2025. For example, the Glo Hilo device in Japan will come with two screens (compared to one in the Serbia version), while the tobacco stick will be more compact.

Following the successful pilot launch in Serbia, BAT and Smoore are working to expand Glo Hilo’s production capacity aggressively and carefully managing the manufacturing footprint to cater to various international markets.

While Smoore provides technical services to BAT regarding tobacco sheet processing, it does not offer the StickSeal technology, which BAT’s in-house R&D team may develop.

While the latest tobacco stick with Stick Seal technology removes the need to clean the device regularly, some users still complain about leakage of “juice” from the used tobacco stick. This is mainly because the tobacco stick is stored for too long and becomes humid. Recognising this issue, Smoore has suggested that BAT educate its consumers to buy no more than one month’s supply each time, as the shelf life of tobacco sticks should not be longer than that.

Besides Glo Hilo, here are management’s comments on the vapour category.

How does the U.S. tariff on Chinese imports affect Smoore’s export to BAT?

In 2018, the Trump administration also imposed tariffs on Chinese imports. At the time, the price increase was passed on to consumers.

Since then, Smoore has diversified its manufacturing footprint to Southeast Asia to mitigate the impact of tariffs.

In any event, the profit margin earned by Smoore, BAT, and retailers in the U.S. (convenience stores, vape shops) shall remain intact, and tariffs (if any) will be passed on to end customers.

The U.S. ITC issued a limited exclusion order against NJOY due to JUUL’s patent infringement case against NJOY. NJOY will be prohibited from sales in the U.S. as early as 31 Mar. How does it affect Smoore’s U.S. shipment volume?

NJOY only accounts for a single-digit percentage of Smoore’s U.S. shipment volume, so the impact will be immaterial.

Smoore is working with Altria to modify the product and relaunch NJOY ACE, but there is no concrete timetable.

Since disposable vapes began gaining traction globally, Smoore management has had numerous discussions on approaching this emerging category. Based on feedback from BAT and Smoore’s judgement, they believe that such a product format has an undesirable environmental impact due to the disposal of batteries. E-cigarettes are a heavily regulated industry, and they were concerned that if the business became sizeable, it would attract more stringent regulatory scrutiny. It is not worth committing significant resources if the business does not reach a large scale. They then adopted a more disciplined approach to launching disposable vape products in Europe but could never achieve market leadership due to limited investment. Since disposable vapes are banned in several European countries, it is too late to invest in this category. The optimal strategy shall be to convert disposable vape customers to pod-based (through its ODM customers such as BAT, as evidenced by the launch of Vuse Go Reload targeting to convert disposable vape customers) and open-system vaping (through their brand Vaporesso).

As disposable vaping products gradually exit the European market, user demand is shifting towards compliant pod-based and open-system products. ODM revenue from Europe declined by -15.7% year over year in 1H 2024 but grew by +14.2% year over year in 2H 2024.

With the FDA strengthening enforcement against non-compliant vaping products, sales revenue in the U.S. resumed year-on-year growth in the second half of 2024. ODM revenue from the U.S. declined by -9.7% year over year in 1H 2024 but grew by +5.1% year over year in 2H 2024. (note: BAT vapour volume in the U.S. declined by 8% yoy in 1H 2024 and increased by 1% yoy in 2H 2024, in line with shipment volume from Smoore)

Their open-system vaping brand, Vaporesso, has grown enormously in recent years despite the category only growing at a single-digit percentage. They have consistently gained market share and become the #1 brand in the U.S. and Europe. Smoore attributed this to the talent density within the company and substantial resources committed to the category. This gives them confidence that they can achieve great results if they have the right talent and commit enough resources to the HNB category.

Delegating responsibility and decision-making to the individual business line will help the organisation become more agile and minimise the risk of management missteps at the group management level.

Conclusion

After the event, I mingled with other analysts and found that some had conducted due diligence by flying to Serbia to try the product and listen to customer feedback. Customer feedback seems to be consistent with management’s analysis. However, it is still too early to tell whether Glo Hilo can be competitive in other larger markets, such as Japan and Italy, let alone challenging IQOS Iluma’s market leadership. (I won’t read too much into anecdotal evidence in this regard.) Even feedback from actual users may vary based on Reddit discussion. (Do real users in Serbia even share their feedback on Reddit? Or perhaps other social media platforms?)

We will only know the outcome in 2H 2025 when Glo Hilo is launched in more international markets, but rest assured that BAT and Smoore are not adopting a cookie-cutter approach to launch it globally. Still, other parameters, such as customer sourcing (i.e., potential cannibalisation versus market share gain), retention rate, and product launch by competitors, will affect revenue growth and product lifecycle (which affect capex and R&D spending as % of revenue structurally). To put it in perspective, Glo Hyper was a good product in 2020-2021 but not good enough to withstand the competition from IQOS Iluma since 2022.

As I mentioned in my previous articles, Smoore has many more proprietary technology IPs in heated tobacco than Glo Hyper or Glo Hilo encompass. They have established an HNB technology platform called Metex that targets ODM customers such as BAT (link to Metex website). Glo Hilo and Glo Hilo Plus are based on induction heating technology, which may license technology IPs from Smoore’s Arch platform and MELUX PE platform, respectively. Below is a comparison of Glo Hilo and Glo Hilo Plus versus Arch and MELUX PE, as you may find some similarities in the design.

Source: BAT FY24 results presentation

Arch (possibly some technology IPs licensed by Glo Hilo)

MELUX PE (possibly some technology IPs licensed by Glo Hilo Plus)

Metex’s innovative design includes many features and innovations, such as ID/CMF (industrial design/colour, material, finishing), usability and UI/UX (user interface/user experience) highlighted below.

Source: Metex official website

Source: Metex official website

Source: Metex official website

The good news is that Glo Hilo has a lot of room to improve by leveraging Metex. The bad news is that Smoore could offer its proprietary HNB technology to BAT’s competitors.

I hope you enjoy reading this article. Please feel free to share anything you hear from Europe or the U.S.

Thanks for reading Recital! Subscribe for free to receive new posts and support my work.

Did the management give any specifics on timing for entering Japan and Italy as well as regulatory approvals for those markets? Or just saying it will happen in H2/2025?

Did the management give any specifics on timing for entering Japan and Italy as well as regulatory approvals for those markets? Or just saying it will happen in H2/2025?

Awesome write up

IQOS is still a different level of brand recognition

Especially in Japan

IQOS store for example hits different